In the sweet spot for global small caps? Investor questions answered

Global small caps offer investors long-term returns potential. Here we summarise the views of our small cap experts in response to key questions from investors at a recent panel session in London.

8 minute read

Key takeaways:

- Small caps are trading at significant discounts relative to their historical averages, indicating a potential undervaluation.

- The current valuation discounts present a catch-up trade opportunity for investors, presenting an opportune time to invest in the asset class.

- Investors should closely monitor small cap valuations and macroeconomic indicators, with the historical performance following rate cuts providing a strategic window for entering the market.

Over the longer term, smaller companies (small caps) have consistently outperformed their large cap counterparts when held for any significant period in portfolios. But why? This was the subject of a recent panel session hosted by our small cap experts, including Richard Brown, Neil Harmon, Rory Stokes, and Nick Sheridan.

Why does small outperform big?

Why do small caps outperform their larger counterparts over the long term? The answer lies in their higher growth potential and room for expansion. Small caps have more room to grow as they are less mature, not as globally present, and have not yet fully explored adjacent product markets.

For example, the challenge US tech giant Apple has in doubling its US$400 billion in annual sales is far greater than a German industrial company with a strong product and newer markets aiming to double its US$2 billion in revenues. Simply, the different scales highlight the mathematical advantage smaller companies have over their mega cap counterparts over the long term. This trend holds true globally (Figure 1) and is evident for the UK and Europe too. The US has bucked this trend, with small caps neglected due to the influence of mega-cap technology stocks like Nvidia and the prevailing artificial intelligence (AI) narrative.

Figure 1: Long-term record of outperformance of small versus large caps

Source: Refinitiv Datastream, Price indices, Janus Henderson Investors Analysis, as at 30 June 2024. Past performance does not predict future returns.

Note: Indices used: MSCI World Small Cap and MSCI World Large Cap; MSCI Europe Small Cap and MSCI World Large Cap; Deutsche Numis Smaller Companies ex Investment Trusts and FTSE 100; Russell 2000 and S&P 500.

Investor question: Where’s the actual catalyst in terms of capital flowing into small cap in the UK? Everyone agrees the small cap space is cheap and attractive, but there feels like there are headwinds that are almost unabated.

We’ve observed a variety of sources thinking about allocating in the UK space, including pension funds, private individuals, private clients, and wealth managers. There’s also hope and an expectation that the government might promote and increase the ownership of UK equities by pension funds. This direction of travel backs up our view that there is a significant opportunity for investors in this sector, as it’s currently very undervalued. The mix of fear and greed has also influenced the market; not being involved in UK small cap in the last couple of years hasn’t been an issue. However, as we start to see profits generated again, I anticipate much more interest in this area. – Neil Hermon, Portfolio Manager

Diversification benefits

Diversifying into small caps benefits investors due to their different sectoral exposures. It also plays into the geopolitical shift to nearshoring of previously global supply chains (Figure 2). Smaller companies tend to have more exposure to sectors such as industrials and materials, and less to technology. This contributes to their cyclicality. Despite current uncertainties in the economic cycle, this has historically worked in small caps’ favour over the long term.

Figure 2: Navigating global disruption – More beneficiaries of nearshoring of supply chains and greater diversification

Source: Bloomberg, Janus Henderson Investors Analysis, as at 30 June 2024.

Many investors are heavily invested in the S&P 500’s top companies. By adding small caps to the mix, investors can gain exposure to different structural themes such as nearshoring, deglobalisation, and the rebuilding of production lines, potentially offering something unique to portfolios. Put simply, adding small caps to an equity portfolio can result in more balanced returns over time due to their differing performance cycles.

M&A tailwinds

Another compelling reason to invest in small caps is the mergers and acquisitions (M&A) tailwind, which is prevailing and persistent across different regions. The vast majority of M&A activities involve a small cap being acquired, usually at a bid premium, which has averaged 38% in 2024. Further, about 95% of all deals involve the purchase of a small cap stock.1

Investor question: Janus Henderson owns smaller companies based on the belief that they have strong potential. But if you get takeover offers and accept them, aren’t you missing out on future gains?

It’s about relative valuations. If you can take that premium and reinvest it elsewhere, there’s more upside potential in the portfolio. However, we have turned down a bid that offered a 30% premium in recent months because we believe the company is worth twice that amount, and as a result, that bid failed. You experience a bit of pain on that day, but fundamentally, we’re trying to maximise the value of the assets for our clients. – Rory Stokes, Portfolio Manager

Undervalued and out of favour

Looking at small cap valuations, based on 12-month forward price to earnings, it’s clear that small caps are currently undervalued and out of favour. This divergence in returns through the summer suggests a pent-up demand for small caps, which are trading at significant discounts compared to their long-run averages: 10% in the UK, 17% in Europe, and slightly less on a global stage at 5% (Figure 3).

Figure 3: Small cap valuations

Source: DataStream, MSCI regional Small Cap indices, Janus Henderson Investors Analysis, as of 12 September 2024.

Note: Forward price to earnings (forward P/E) is a version of the ratio of price to earnings (P/E) that uses forecasted earnings for the P/E calculation.

These valuations versus large caps shows that small caps are trading at substantial discounts, indicating a potential catch-up trade once there is some level of stabilisation in the economy.

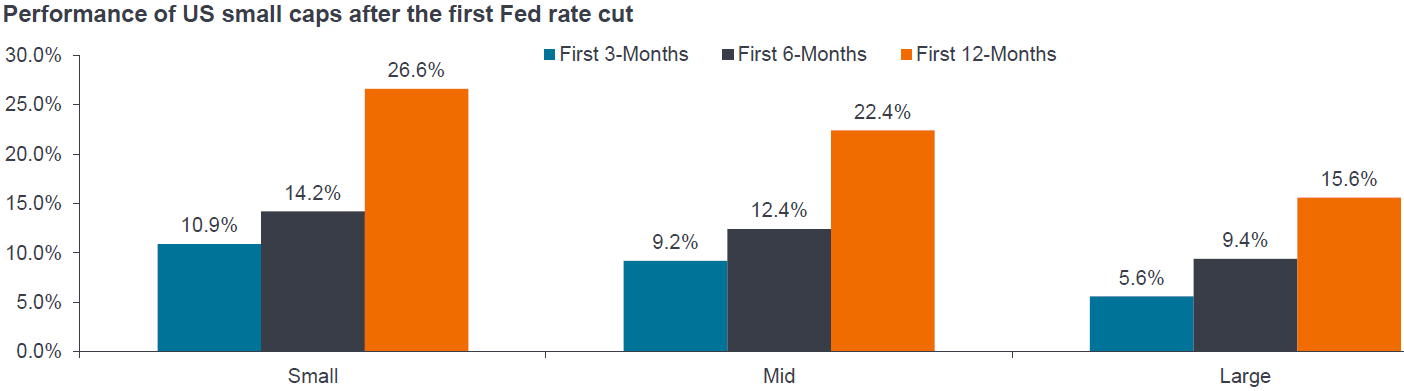

Rate cuts are also good news for small caps. Historical data from the US shows that small caps have typically seen a 26% return in the 12 months following the first rate cut of a cycle (Figure 4).

Figure 4: Small cap after a Fed cut

Source: Federal Reserve Board, Haver Analytics, Center for Research in Security Prices (CRSP), University of Chicago Booth School of Business, Jefferies, Janus Henderson Investors Analysis.

Note: Used Fed Funds rate from 1954 until 1963, then used Discount rate from 1963 until 1994 and Fed Funds rate after that. Past performance does not predict future returns.

Why does this happen?

- P/E expansion due to expectations of profit growth from small caps which is more sensitive to GDP.

- A disproportionate reduction in borrowing costs for small caps relative to large caps.

- Lower market volatility/business uncertainty is reflected in reduced liquidity concerns, which stimulates institutional demand in a more illiquid asset class.

- Lower borrowing costs stimulate M&A activity.

Investor question: What keeps you up at night? What do you worry about most from a small cap investment perspective looking ahead over the next 12 months?

Whatever we worry about is not likely to be the thing that ultimately impacts us, because it’s unlikely we, and the wider investing world, will actually see it coming. We have to be ready for surprises. However, I am concerned about policy issues and the loss of the peace dividend, which doesn’t seem to be resolving itself. AI, I think, is incredibly worrying for the employment of a certain generation, even though it might be beneficial for another. Ultimately, share prices climb a wall of worry because people stand back. Fear and greed, by definition, dislocate share prices away from their fundamental value. Therefore, the more fearful people become in the short term, the better it can be for long-term investment, provided you’re prepared to put your money where your mouth is. We believe an active management approach to small caps puts investors in a strong position to benefit. – Nick Sheridan, Portfolio Manager

IMPORTANT INFORMATION

References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance cannot guarantee future results.

There is no guarantee that past trends will continue, or forecasts will be realised.

Smaller capitalisation securities may be less stable and more susceptible to adverse developments, and may be more volatile and less liquid than larger capitalisation securities.

MSCI Europe Small Cap captures small cap representation across the Developed Markets (DM) countries in Europe. The index covers approximately 14% of the free float-adjusted market capitalisation in the European equity universe.

MSCI Europe Large Cap captures large cap securities exhibiting overall value style characteristics across 15 developed markets countries in Europe.

Deutsche Numis Smaller Companies (ex-Investment Trusts) is a measure of the combined performance of smaller companies (the bottom 10%) listed on the London Stock Exchange excluding investment companies. It provides a useful comparison against which the Fund’s performance can be assessed over time.

FTSE 100 is comprised of the 100 most highly capitalised blue chips listed on the London Stock Exchange.

Russell 2000 is a stock market index that measures the performance of the 2,000 smaller companies included in the Russell 3000 Index.

S&P 500 is a market-capitalisation-weighted index of 500 leading publicly traded companies in the US.

MSCI World Small Cap captures small cap representation across 23 developed markets. With over 4,000 constituents, the Index covers approximately 14% of the free float-adjusted market capitalisation in each country.

MSCI World Large Cap captures large cap representation across 23 developed markets countries. With 614 constituents, the index covers approximately 70% of the free float-adjusted market capitalisation in each country.

1Source: Bloomberg, Factset, J.P. Morgan calculations, Janus Henderson Investors Analysis, as of 30 June. Note: Stocks below US$100m market cap excluded.

Cyclical stocks: Companies that sell discretionary consumer items (such as cars), or industries highly sensitive to changes in the economy (eg. mining).

Discount: Refers to a situation when a security is trading for lower than its fundamental or intrinsic value. The opposite of trading at a premium.

Diversification: A way of spreading risk by mixing different types of assets/asset classes in a portfolio, on the assumption that these assets will behave differently in any given scenario. Assets with low correlation should provide the most diversification.

Economic cycle: The fluctuation of the economy between expansion (growth) and contraction (recession), commonly measured in terms of gross domestic product (GDP). It is influenced by many factors, including household, government and business spending, trade, technology and central bank policy. The economic cycle consists of four recognised stages. ‘Early cycle’ is when the economy transitions from recession to recovery; ‘mid-cycle’ is the subsequent period of positive (but more moderate) growth. In the ‘late cycle’, growth slows as the economy reaches its full potential, wages start to rise and inflation begins to pick up, leading to lower demand, falling corporate earnings and eventually the fourth stage – recession.

Large caps: Well-established companies with a valuation (market capitalisation) above a certain size, eg. $10 billion in the US. It can also be used as a relative term. Large-cap indices, such as the UK’s FTSE 100 or the S&P 500 in the US, track the performance of the largest publicly traded companies, rather than all stocks above a certain size.

Macroeconomics/Microeconomics: Macroeconomics is the branch of economics that considers large-scale factors related to the economy, such as inflation, unemployment or productivity. Microeconomics is the study of economics at a much smaller scale, in terms of the behaviour of individuals or companies.

Mega caps: The largest designation for companies in terms of market capitalisation. Companies with a valuation (market capitalisation) above $200 billion in the US are considered mega caps. These tend to be major, highly recognisable companies with international exposure, often comprising a significant weighting in an index.

Share price: The price to purchase (or sell) one share in a company, not including fees or taxes. For investment trusts: The closing mid-market share price at month end.

Small caps: Companies with a valuation (market capitalisation) within a certain scale, eg. $300 million to $2 billion in the US, although these measures are generally an estimate. Small cap stocks tend to offer the potential for faster growth than their larger peers, but with greater volatility.

Volatility: The rate and extent at which the price of a portfolio, security or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. The higher the volatility the higher the risk of the investment.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Shares of small and mid-size companies can be more volatile than shares of larger companies, and at times it may be difficult to value or to sell shares at desired times and prices, increasing the risk of losses.

- The Fund may use derivatives with the aim of reducing risk or managing the portfolio more efficiently. However this introduces other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

Specific risks

8 minute read

Key takeaways:

- Small caps are trading at significant discounts relative to their historical averages, indicating a potential undervaluation.

- The current valuation discounts present a catch-up trade opportunity for investors, presenting an opportune time to invest in the asset class.

- Investors should closely monitor small cap valuations and macroeconomic indicators, with the historical performance following rate cuts providing a strategic window for entering the market.