Key takeaways:

- Non-U.S. stocks have been the underdogs of global markets for more than a decade, but changing geopolitics are helping lift the prospects of some foreign companies.

- Defense companies are one example, as European governments announce plans to accelerate defense spending in response to the U.S. likely pivoting toward the Pacific and away from Europe.

- Among European defense firms, investors could find attractive growth, along with an opportunity to diversify U.S.-centric equity portfolios.

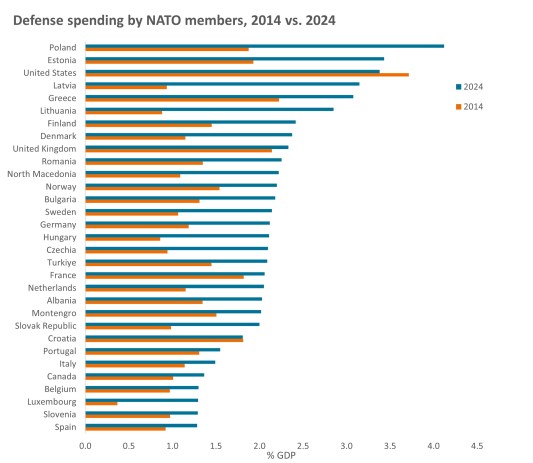

Source: NATO, Defence Expenditure of NATO Countries (2014-2024), 17 June 2024. GDP=gross domestic product. NATO=The North Atlantic Treaty Organization, an intergovernmental transnational military alliance of 32 member states (30 European and two North American). Data excludes Iceland, which has no armed forces.

For decades, defense budgets in Europe experienced little to no growth. But amid new geopolitical tensions and a change in White House leadership, defense spending in the region is poised to accelerate.

Already, countries located near Russia have dramatically increased defense expenditures as a percentage of their gross domestic product (GDP), with Poland committing more than 4% of its GDP in 2024, up from less than 2% a decade ago. More recently, Ursula von der Leyen, president of the European Commission, said the EU plans to activate a mechanism that allows member states to substantially increase defense expenditures without having to make cuts elsewhere. She also proposed lending up to 150 billion euros (US$158 billion) to EU governments to rearm amid worries about faltering U.S. support for Ukraine.

Some countries have already taken action. This year, the UK pledged to increase its defense spending from an estimated 2.3% of GDP in 2024 to 2.5% by 2027 (and target a 3% level in subsequent years) and Denmark announced it would boost its defense spending to more than 3% of GDP in 2025 and 2026. In addition, Germany’s incoming government recently said it will launch a 500 billion euro ($528 billion) fund to invest in infrastructure projects and that it will amend the constitution to exclude defense outlays from fiscal spending limits.

The shift in policy has helped to lift non-U.S. defense stocks. Until recently, though, many of the shares traded at valuations that reflected much lower rates of growth. One possible reason: After more than a decade of U.S. outperformance, market participants have seemingly written off foreign stocks. But amid a changing geopolitical backdrop, investors may want to reconsider.

We’re standing at a turning point for fiscal, trade, and defense policy, and believe the resulting volatility is creating disconnects investors can take advantage of. Defense is one example. Outside the U.S., the industry has historically been very slow growing. But as geopolitical alliances shift, we expect non-U.S. defense revenues to accelerate, and we think markets are only beginning to catch up to this potential for faster growth. – Julian McManus

Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility, lower liquidity and differing financial and information reporting standards, all of which are magnified in emerging markets.

Volatility measures risk using the dispersion of returns for a given investment.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Emerging markets expose the Fund to higher volatility and greater risk of loss than developed markets; they are susceptible to adverse political and economic events, and may be less well regulated with less robust custody and settlement procedures.

- The Fund may use derivatives with the aim of reducing risk or managing the portfolio more efficiently. However this introduces other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.