Key takeaways:

- Inflation among developed markets had tended to be synchronous since the initial COVID shock but something odd has emerged in the UK during 2023, which has caused UK inflation to be stubbornly higher and similarly gilt yields.

- Explanations for the inflation conundrum range from benign/temporary reasons through to potentially more persistent inflation.

- For international investors, there are potentially easier markets in which to invest, where the inflation outlook offers an earlier return to normality and the potential for rate cuts.

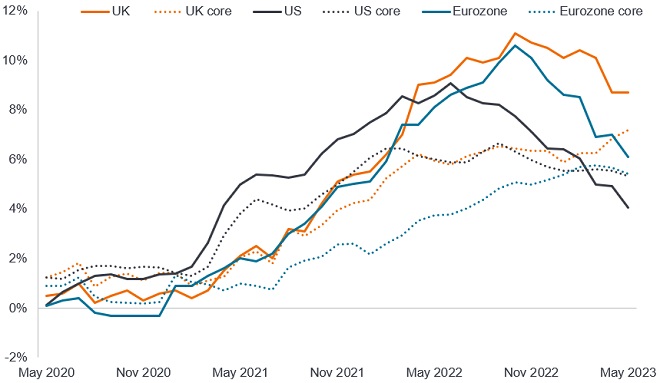

The experience of inflation among developed markets tended to be synchronous since the initial COVID shock but something odd has emerged in the UK during 2023.

Nearly all developed markets experienced a period of low inflation following the 2007-9 Global Financial Crisis (GFC). This came to a rude halt as a combination of monetary and fiscal stimulus to counter the economic effects of COVID lockdowns melded with the supply shocks caused by the war in Ukraine in 2022. Inflation rates of 9-11% – levels not seen since the 1980s – made headlines. While inflation peaked and has come down rapidly in recent months across both emerging and developed markets, in the UK it has proved much more stubborn. Specifically, core inflation has continued to rise in recent months causing a profound crisis of confidence in UK monetary policy.

A regime shift

In the decades before the GFC, UK gilts had typically yielded more than US government bonds and German government bonds. Post the Brexit vote, gilt yields tended to be lower, sitting midway between US government bond yields and German government bond yields. In 2023, they have decisively broken out of this regime and returned to being the highest yielding of the three countries.

Various factors might explain this. Among them are the UK’s large fiscal deficit and its composition (the UK government needs to issue a lot of gilts and has a relatively high number of index-linked gilts that have to pay out more when inflation is higher). Faded appetite from buyers for gilts after recent political upheavals has also not helped. But most important in 2023 is the inflation outlook. The conundrum is why should core inflation have continued to rise at alarming rates in the UK?

Fig 1: Inflation rates across the UK, the US and the Eurozone

Source: Refinitiv Datastream, Consumer Price Index, year-on-year % change, headline inflation in bold lines, core in dotted lines, 31 May 2020 to 31 May 2023. Core inflation excludes energy and food in the US and additionally alcohol and tobacco in the UK and the Eurozone.

Core inflation (which excludes the volatile items of food and energy) typically lags headline inflation. In the US, it is likely to come down further as we know what wholesale used car prices and market rents are doing and these feed into official inflation statistics with a lag. In the UK bizarrely, it is not just services but core goods prices have started reaccelerating and core inflation is still ticking up as a result.

There are a number of ways to try and explain the UK inflation conundrum ranging from benign/ temporary explanations to one of a much more problematic persistent inflation problem.

Be patient

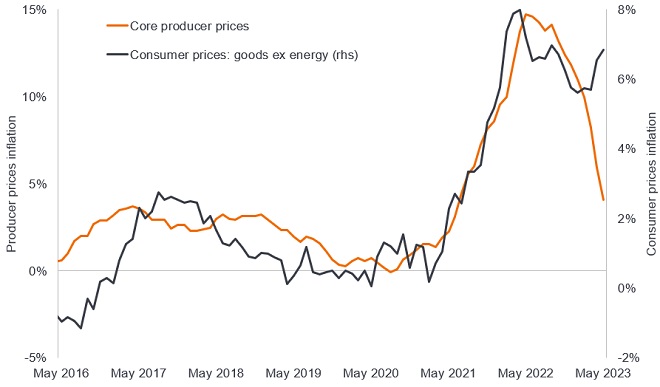

The first is it may be down to time lags and measurement quirks so no need to panic. If we look at producer price indices, these are coming down swiftly and are likely to follow through into consumer prices (although recent profit margin expansion and pass through of exchange rate costs disrupted the downward trajectory). The energy price cap drops are likely to feed into drops in the July data when it is released in August. Monthly core inflation prints are subject to huge overshoots/undershoots in either direction and it will take time to assess the true trend.

Fig 2: Core consumer goods inflation curiously ticked up as producer prices moderate

Source: Refinitiv Datastream, UK Producer Price Index: output prices ex food, beverages, tobacco and petroleum; UK Consumer Price Index: non-energy goods, year-on-year % change, 31 May 2016 to 31 May 2023.

UK inflation has been brought forward

The second is the notion that inflation was sucked into the first half of this year. Firms that set prices in response to events are referred to as “state dependent” whilst those that change prices at regular fixed intervals e.g. annually are described as “time dependent”. The Bank of England’s Decision Maker Panel (DMP) Survey of firms noted that state dependent price setting firms have been raising prices more than time dependent firms. Companies may have pushed through prices while they could in the expectation inflation would be softer later in the year. Encouragingly, when asked about price rises for next year, state dependent firms (which make up about 60% of firms) predicted lower inflation than time dependent price setters.

A persistent inflation problem

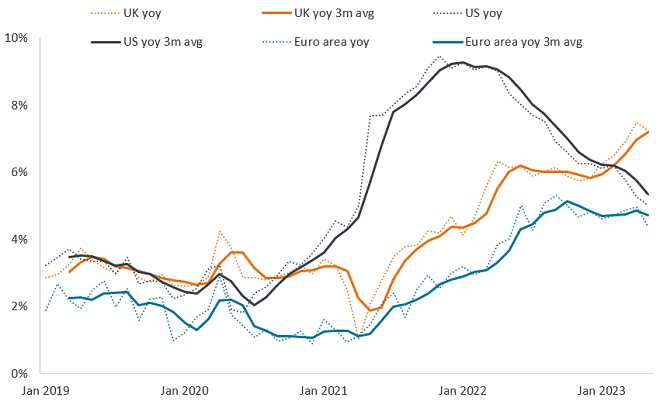

The third is that the UK has become unhinged from the US and Europe and has more persistent inflation. Reasons might be due to greater trade friction post Brexit leading to higher costs and a peculiarly tight labour market. While wages in the US and Europe are moderating, this is not yet evident in the UK.

Fig 3: Wage growth in UK is still accelerating while moderating elsewhere

Source: Indeed Wage Tracker, January 2019 to May 2023. Yoy = year-on-year % change. The euro area series is an employment-weighted average of France, Germany, Ireland, Italy, Netherlands, and Spain. The 3-month average compares a 3-month period with the same 3-month period a year ago to smooth out distortions in an individual month.

Such profound uncertainty sourced from a lack of true understanding about what is driving UK inflation has caused a crisis of confidence on the interest rate outlook. UK peak rate expectations surged higher in early July on little/no meaningful economic data, reaching over 6.5%.1 A sudden concern that interest rates may be having little impact on the UK economy created this airpocket in rate expectations. This argument ignores lags inherent in monetary policy but reveals the crisis of confidence surrounding UK monetary policy at present. Last October, the crisis of confidence was of course about fiscal policy.

Overseas preference

Given the uncertainty surrounding the drivers of UK core inflation for most international investors there are much easier bond markets in which to invest. This includes economies where the inflation story is showing the potential for a return to normality, albeit for core inflation this will still take some time as it typically lags. In emerging markets there are already nascent debates about the first rate cuts, while for most central banks in the developed world the debate is about the last rate hike or two in this cycle. Sitting in the UK, the global covid inflation shock can look very different to other economies e.g. China where CPI inflation has hit 0% in June 2023 or the US down to 3% (from 9.1% a year ago).2

1Source: Bloomberg, interest rate projections, correct at 6 July 2023.

2Source: Refinitiv Datastream, China CPI inflation, US CPI inflation for June 2023, as at 12 July 2023.

Gilts: Government bonds issued by the UK government to finance UK national debt. Index-linked gilts have coupon (interest payments) and final maturity value (amount repaid on the date the bond matures) that are adjusted in line with the inflation rate.

Inflation: The rate at which the prices of goods and services are rising in an economy. Headline inflation refers to inflation across all goods and services, whereas core inflation excludes components that exhibit large amounts of volatility from month to month such as fuel and food prices.

Monetary policy: The policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money.