Key takeaways:

- Recent acquisitions of listed residential REITs by major private real estate operators like Blackstone highlight the significant opportunity created by the listed versus private valuation gap and the constructive long-term outlook for listed real estate.

- The listed residential sector has generated attractive long-term returns driven by supportive demographic trends, an undersupply of housing in most global markets (something likely to be accentuated in the years ahead), and a desire for affordable and well-managed rental homes.

- Relative to other property types, US residential assets benefit from lower debt pricing and availability, backed by government-supported debt markets, limited sales, and lower distress levels.

As we have highlighted before, the private commercial real estate market has dominated media headlines and has been slow to adjust reported values as the macroeconomic background changes. This is the opposite for the listed/public market, which is forward looking, being priced daily in stock markets, with valuations very much already reflecting the negative impact of higher rates on underlying property values. This means listed real estate investment trusts (REITs) are trading at wide discounts to private asset values having already “priced in” the impact of higher rates, and today stands to benefit from a reversal in the direction of interest rates.

How do we evidence this? One key indicator is that the private real estate sector is taking advantage of the significant valuation gap between private and listed real estate, to reap the existing value in listed REITs today. Recently, Blackstone, the largest private operator announced it is acquiring listed upscale coastal apartments REIT, Apartment Income (AIR Communities), for approximately US$10 billion. This follows on from an earlier acquisition this year, Canadian REIT Tricon Residential, a portfolio of mainly single-family homes in the US Sunbelt region in January for US$3.5 billion. With both deals struck at more than a 20% premium to the prevailing share prices, we see this as illustrative of the attractive pricing of listed residential REITs (and the wider listed REIT sector).

Still compelling valuations

Looking specifically at US residential REITs (Figure 1), the sector still looks undervalued compared to observed private market pricing from recent transactions. Apartment REITs are currently trading at around 10% discounts to estimated net asset value (NAV), while single family rental REITs illustrate an even wider discount of circa 20%.

Over in Europe, we see German residential landlords trading at discounts of around 40% to appraised values, reflecting higher leverage (debt levels), but also in our view creating an opportunity for investors.

Figure 1: US residential average NAV premium/discount

Source: SNL Real Estate, Janus Henderson Investors. Data from 31 December 2005 to 31 March 2024. NAV or net asset value: value of REIT underlying assets minus liabilities. Premium to NAV: REIT price is higher than its NAV; discount to NAV: REIT price is lower than its NAV. Past performance does not predict future returns.

While we expect peak-to-trough valuation declines for commercial real estate of circa 20% from early 2022 highs, the residential sector may likely see valuations stabilise quicker than many other sectors, being a relative beneficiary from investors’ reduction of exposure to the more challenging segments of commercial real estate, such as office and low-quality shopping centres.

Well placed for growth

Since the 2008 Global Financial Crisis, listed residential REITs have reduced leverage, positioning themselves favourably entering the recent downturn, notably in the US. This lower leverage can allow for superior access to funds at a lower cost compared to private owners. We expect listed REITs to put their cost of and access to capital advantages to good use and acquire “good buildings with bad balance sheets” from private owners. This could increase the potential for the asset class to continue expanding market share, as they have done over the past three decades, as well as contribute to additional earnings growth.

Furthermore, REITs typically have efficient expense structures coupled with an ability to invest in operating platform improvements, which has often resulted in higher occupancy levels, higher achieved rents, and more efficient operating margins compared to their private peers. In early 2024 some US landlords have achieved around 95% occupancy levels, with mid-single-digit uplifts on tenant lease renewals.

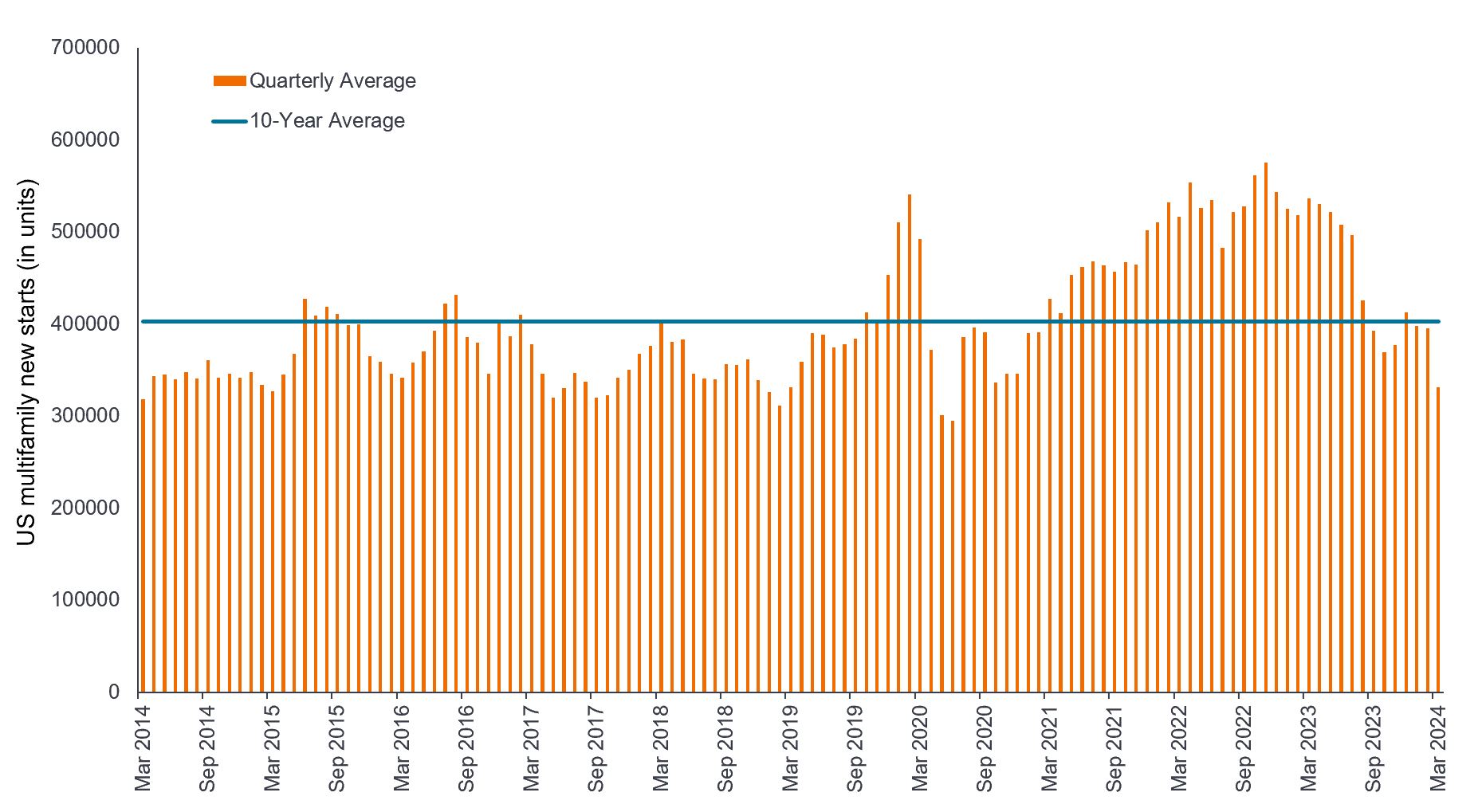

While elevated supply looks to be a short-term headwind for US apartments, construction activity is now slowing dramatically, which should also aid medium-term growth prospects.

Figure 2: New construction starts below 10-year average

US Multifamily new starts (annualised, seasonally-adjusted)

Source: US Census Bureau, Janus Henderson Investors, 31 March 2014 – 31 March 2024.

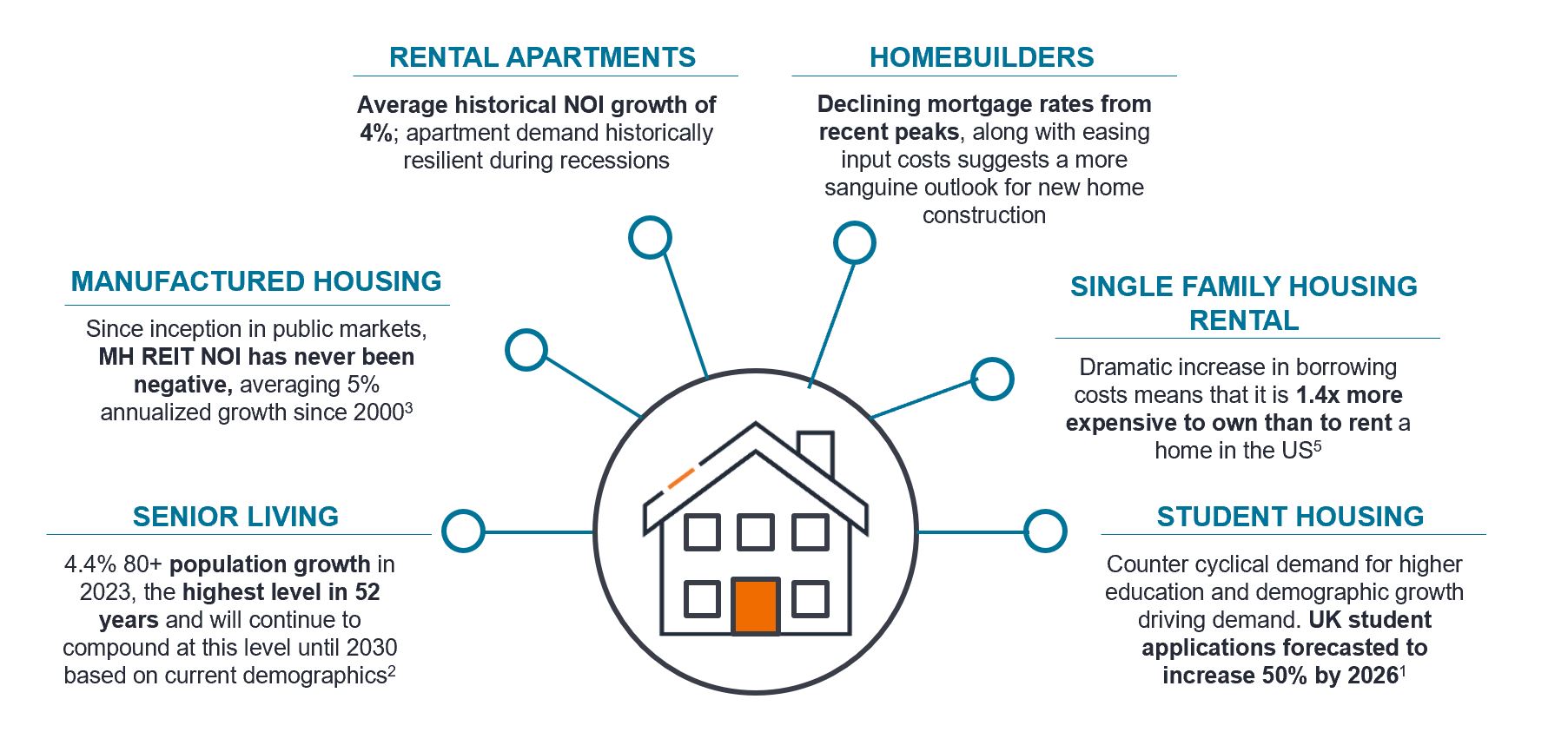

Residential: a diverse sector with defensive characteristics

The listed residential sector has proven it can generate attractive long-term returns and income streams, which have historically tended to keep pace with inflation. The listed market also offers a broader opportunity set. Areas such as student accommodation, single-family housing rentals, retirement communities and senior living, all have benefited from structural demand drivers such as the demographic trend of an ageing population.

Figure 3: The residential opportunity

Structurally undersupplied across different subsectors

Source: 1UCAS, 2OECD, 3,4Green Street Advisors, 5 Jefferies, FRED, NAR, REIS, Redfin, Janus Henderson Investors analysis, as at 31 December 2022. NOI=net operating income, a measure of an income-producing property’s revenues minus operating expenses (financing and tax).

Selectivity is imperative

We reiterate that a selective approach is key when it comes to investing in the property sector, as multiple factors such as tenant demand, market supply, funding cost and availability among others, can differ widely not only between property types but also at the regional and local level.

The single-family rental sector is arguably best positioned within residential, given its sticky customer base and strong demand trends aided by declining mortgage availability and depressing home purchase activity. In North America, the US East Coast’s fundamentals are stronger due to better job growth and supply compared to the West Coast and the Sunbelt markets. In Canada, we are seeing strong market rent growth supported by Canada’s dynamic immigration policy and healthy employment. Meanwhile in Europe, some Swedish and German residential companies assumed large volumes of debt which in a rising rate environment have seen much weaker valuations. However, we think the operational resilience and robust cash flows of companies in the region are underappreciated by the market and importantly, where leverage levels were too high, companies have used dividend cuts, fresh equity injections and asset disposals to help address these concerns.

The bottom line

Residential REIT markets around the world continue to offer compelling opportunities supported by demographic trends, an undersupply of housing in most global markets (that is likely to be accentuated in the years ahead), and a desire for affordable and well-managed rental homes.

We look ahead with greater confidence and conviction that listed REITs may again prove to be a valuable building block within investors’ portfolios, given its potential for attractive and growing dividend streams, diversification against other asset classes, and defensive growth.

Given Blackstone’s recent acquisitions, we would not be surprised to hear of more acquisitions of listed REITs by private operators in the coming months. This should help build a strong positive outlook for listed real estate and provide confidence to investors to take another look at the sector.

Balance sheet: a financial statement that summarises a company’s assets, liabilities and shareholders’ equity at a particular point in time.

Investment grade: a bond/debt issue that has a relatively low risk of defaulting on its principal and interest payments, reflected in the higher rating given by credit ratings agencies.

Net Asset Value (NAV): the total value of an asset minus outstanding debt and fixed capital expenses.

REITs or Real Estate Investment Trusts invest in real estate, through direct ownership of property assets, property shares or mortgages. As they are listed on a stock exchange, REITs are usually highly liquid and trade like shares.

Real estate securities, including Real Estate Investment Trusts (REITs), are sensitive to changes in real estate values and rental income, property taxes, interest rates, tax and regulatory requirements, supply and demand, and the management skill and creditworthiness of the company. Additionally REITs could fail to qualify for certain tax-benefits or registration exemptions which could produce adverse economic consequences.

Important information

Please read the following important information regarding funds related to this article.

Key investment risks:

- The Fund's investments in equities are subject to equity securities risk due to fluctuation of securities values.

- Investments in the Fund involve general investment, currency, liquidity, hedging, market, economic, political, regulatory, taxation, securities lending related, reverse repurchase transactions related, financial, interest rate and small/ mid-capitalisation companies related risks. In extreme market conditions, you may lose your entire investment.

- The Fund may invest in financial derivatives instruments to reduce risk and to manage the Fund more efficiently. This may involve counterparty, liquidity, leverage, volatility, valuation and over-the-counter transaction risks and the Fund may suffer significant losses.

- The Fund’s investments are concentrated in European property sector (may include small/ mid capitalization companies). It may be more volatile and subject to property securities related risk.

- The Fund may invest in Eurozone and may suffer from Eurozone risk.

- The directors may at its discretion pay distributions out of gross investment income and net realised/ unrealised capital gains while charging all or part of the fees and expenses to the capital, resulting in an increase in distributable income for the payment of distributions and therefore, the Fund may effectively pay distributions out of capital. This amounts to a return or withdrawal of part of an investor's original investment or from any capital gains attributable to that original investment, and may result in an immediate reduction of the Fund’s net asset value per share.

- The Fund may charge performance fees . An investor may be subject to such fee even if there is a loss in investment capital.

- Investors should not only base on this document alone to make investment decisions and should read the offering documents including the risk factors for further details.

Key investment risks:

- The Fund's investments in equities are subject to equity securities risk due to fluctuation of securities values.

- Investments in the Fund involve general investment, currency, liquidity, hedging, market, economic, political, regulatory, taxation, securities lending related, reverse repurchase transactions related, financial and interest rate risks. In extreme market conditions, you may lose your entire investment.

- The Fund may invest in financial derivatives instruments to reduce risk and to manage the Fund more efficiently. This may involve counterparty, liquidity, leverage, volatility, valuation and over-the-counter transaction risks and the Fund may suffer significant losses.

- The Fund’s investments are concentrated in property sector and may be more volatile and subject to property securities related risk.

- The Fund may invest in Eurozone and may suffer from Eurozone risk.

- The directors may at its discretion pay distributions (i)out of gross investment income and net realised/ unrealised capital gains while charging all or part of the fees and expenses to the capital, resulting in an increase in distributable income for the payment of distributions and therefore, the Fund may effectively pay distributions out of capital; and (ii) additionally for sub-class 4 of the Fund, out of original capital invested. This amounts to a return or withdrawal of part of an investor's original investment or from any capital gains attributable to that original investment, and may result in an immediate reduction of the Fund’s net asset value per share.

- The Fund may charge performance fees. An investor may be subject to such fee even if there is a loss in investment capital.

- Investors should not only base on this document alone to make investment decisions and should read the offering documents including the risk factors for further details.

Key investment risks:

- The Fund's investments in equities are subject to equity market risk due to fluctuation of securities values.

- Investments in the Fund involve general investment, currency, hedging, economic, political, policy, foreign exchange, liquidity, tax, legal, regulatory, securities financing transactions related and small/ mid-capitalisation companies related risks. In extreme market conditions, you may lose your entire investment.

- The Fund may invest in financial derivatives instruments for investment and efficient portfolio management purposes. This may involve counterparty, liquidity, leverage, volatility, valuation, over-the-counter transaction, credit, currency, index, settlement default and interest risks; and the Fund may suffer total or substantial losses.

- The Fund's investments are concentrated in companies (may include small/ mid capitalization companies, REITs) engaged in or related to the property industry and may be more volatile and are subject to REITs and property related companies risks.

- The Fund may invest in developing markets and involve increased risks.

- The Fund may at its discretion pay dividends (i) pay dividends out of the capital of the Fund, and/ or (ii) pay dividends out of gross income while charging all or part of the fees and expenses to the capital of the Fund, resulting in an increase in distributable income available for the payment of dividends by the Fund and therefore, the Fund may effectively pay dividends out of capital. This may result in an immediate reduction of the Fund’s net asset value per share, and it amounts to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment.

- Investors should not only base on this document alone to make investment decisions and should read the offering documents including the risk factors for further details.