How did you navigate a challenging year for UK markets?

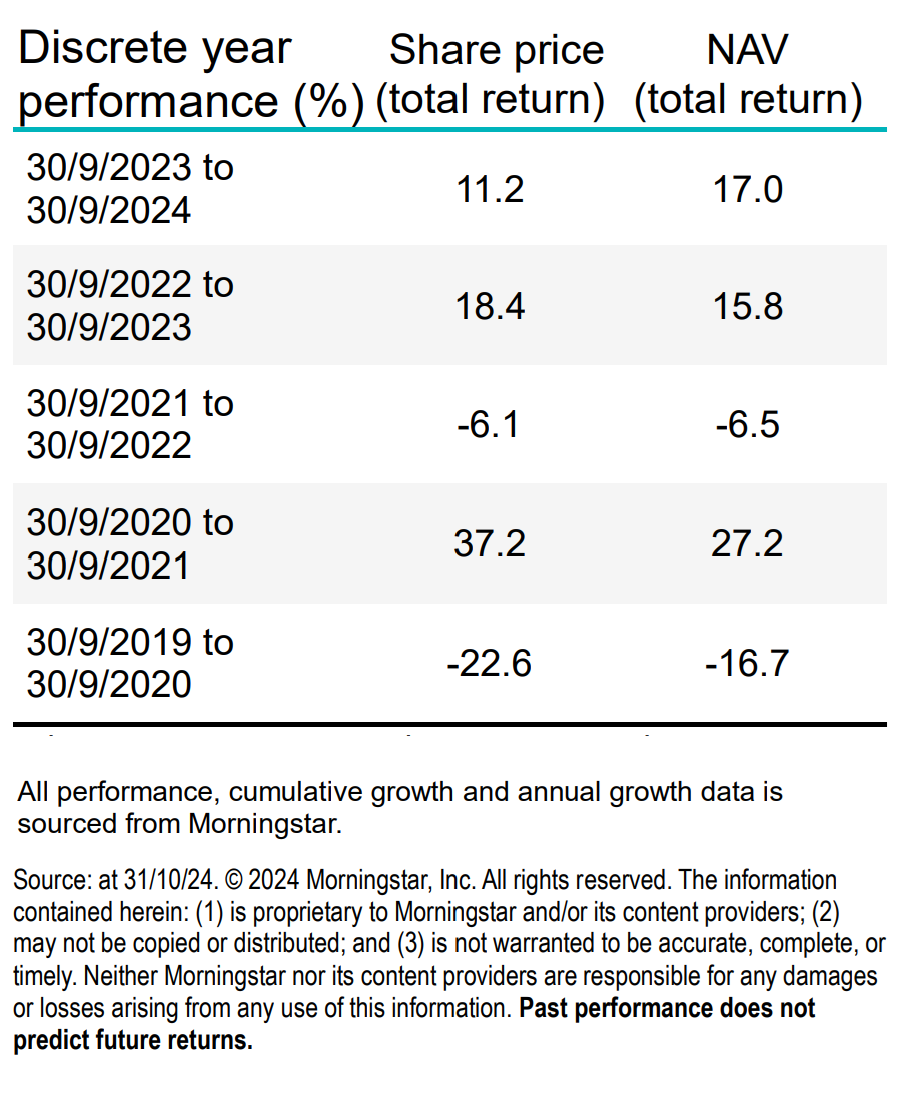

Henderson High Income’s NAV rose 8.8% in the year to 31 August 2024, against the benchmark – 80% FTSE All-Share Index/ 20% ICE BofA Sterling Non-Gilts Index – return of 6.6% in the same period.

The top three contributors to this performance were NatWest, Britvic and Imperial Brands. The three reflected different trends in the market – NatWest from raised interest rates, Britvic from being bid for by Carlsberg and Imperial Brands from the support of share buybacks. The trust also benefitted from being overweight equities vs bonds given the former outperformed.

How did dividends fare in 2024 and what is your outlook for 2025?

The year saw muted growth overall for the UK market in dividends. In particular, strong growth from banks was offset by further dividend cuts in mining. However, the Trust’s income did rise over the year, thanks in part to an overweight to banks.

We expect UK market income to grow between 3% and 5% next year. Financial companies are still seeing good growth and the impact from mining dividend cuts is coming to an end. Despite this, we expect lacklustre dividend growth among domestic companies given the impact from the Budget, particularly the rise in employer national insurance contributions.

What are your expectations for UK interest rates and how are you factoring these into your investing?

We believe that the UK Budget is likely to be inflationary given the increased cost of both wage growth and national insurance rises are likely to be passed on. In that context, we would expect the rate of interest rate cuts to slow. However, we still expect rates to come down given that economic growth is subdued. In our view, the general economic recovery in the UK has been pushed back by a year.

Where we hold companies that are most correlated to interest rates – such as housebuilders, real estate companies and financial services – we have been sticking with them. The pull back in UK markets later in the year means valuations are attractive on a long-term view.

Which areas of the market are most interesting you at the turn of the year?

We are looking for companies with self-help turnaround stories and idiosyncratic underappreciated stories that should create value even if the economic cycle and broader economic backdrop is just okay. Examples in the portfolio include Reckitt Benckiser, DCC and Sodexo.

Glossary

Bond

A debt security issued by a company or a government, used as a way of raising money. The investor buying the bond is effectively lending money to the issuer of the bond. Bonds offer a return to investors in the form of fixed periodic payments (a ‘coupon’), and the eventual return at maturity of the original amount invested – the par value. Because of their fixed periodic interest payments, they are also often called fixed income instruments.

Dividend

A variable discretionary payment made by a company to its shareholders.

Equity

A security representing ownership, typically listed on a stock exchange. ‘Equities’ as an asset class means investments in shares, as opposed to, for instance, bonds. To have ‘equity’ in a company means to hold shares in that company and therefore have part ownership.

Inflation

The rate at which the prices of goods and services are rising in an economy. The Consumer Price Index (CPI) and Retail Price Index (RPI) are two common measures. The opposite of deflation.

Net asset value (NAV) total return (investment trusts)

The theoretical total return on shareholders’ funds per share reflecting the change in Net Asset Value (NAV) assuming that dividends paid to shareholders were reinvested at NAV at the time the shares were quoted ex-dividend. A way of measuring investment management performance of investment trusts which is not affected by movements in discounts/premiums.

Outperform

This has multiple meanings.

To deliver a return greater than that of a portfolio’s assigned benchmark. Also often called excess return.

A rating that can be assigned to a company’s stock by analysts, implying an expectation that the stock will produce better returns than the market (or another relevant benchmark).

Overweight

Having a relatively large exposure to an individual security, asset class, sector, or geographical region than a relevant benchmark, such as an index.

Share price total return (investment trusts)

The theoretical total return to the investor assuming that all dividends received were reinvested in the shares of the company at the time the shares were quoted ex-dividend. Transaction costs are not taken into account.

Disclaimer

References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

There is no guarantee that past trends will continue, or forecasts will be realised.

Past performance does not predict future returns.

Not for onward distribution. Before investing in an investment trust referred to in this document, you should satisfy yourself as to its suitability and the risks involved, you may wish to consult a financial adviser. This is a marketing communication. Please refer to the AIFMD Disclosure document and Annual Report of the AIF before making any final investment decisions. Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Tax assumptions and reliefs depend upon an investor’s particular circumstances and may change if those circumstances or the law change. Nothing in this document is intended to or should be construed as advice. This document is not a recommendation to sell or purchase any investment. It does not form part of any contract for the sale or purchase of any investment. We may record telephone calls for our mutual protection, to improve customer service and for regulatory record keeping purposes.

Issued in the UK by Janus Henderson Investors. Janus Henderson Investors is the name under which investment products and services are provided by Janus Henderson Investors International Limited (reg no. 3594615), Janus Henderson Investors UK Limited (reg. no. 906355), Janus Henderson Fund Management UK Limited (reg. no. 2678531), (each registered in England and Wales at 201 Bishopsgate, London EC2M 3AE and regulated by the Financial Conduct Authority), Tabula Investment Management Limited (reg. no. 11286661 at 10 Norwich Street, London, United Kingdom, EC4A 1BD and regulated by the Financial Conduct Authority) and Janus Henderson Investors Europe S.A. (reg no. B22848 at 78, Avenue de la Liberté, L-1930 Luxembourg, Luxembourg and regulated by the Commission de Surveillance du Secteur Financier).

Janus Henderson is a trademark of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc