Key takeaways:

- While virtually all aspects of President Trump’s April 2 global tariffs announcement remain unclear, what is less uncertain is that tariffs are likely to be bad for economic growth, consumers, and markets.

- Perhaps the most important question is whether a global trade war can push this late-cycle economy into a global recession. While we think the answer is still “no,” US equities remain relatively expensive and therefore potentially sensitive to negative surprises.

- However, it is also worth noting that stimulative policy in Europe and China has the potential to combine with forthcoming stimulative US policy to create a fertile medium-term environment for active investors. Staying invested with a well-balanced portfolio may therefore be the best way to weather current volatility.

“Liberation Day” may or may not free markets from the tightening bind that they find themselves in with respect to US trade policy. Investors and company management dislike uncertainty, and the piecemeal, unreliable way in which tariff announcements are being delivered is creating plenty of it.

Wednesday looks set to bring a wide range of tariffs, but everything – from the scale to the timing to the variability across countries – still seems somewhat up in the air. Estimates on what the average tariff rate will look like range from a few percentage points in moderate outcomes to double-digit levels in more forceful scenarios. It also remains unclear to what extent tariffs are a negotiating strategy to attain some other goal versus being the objective end state. What does seem less uncertain is that tariffs are, without much exception, likely to be bad for economic growth, consumers, and markets.

Consumer concerns

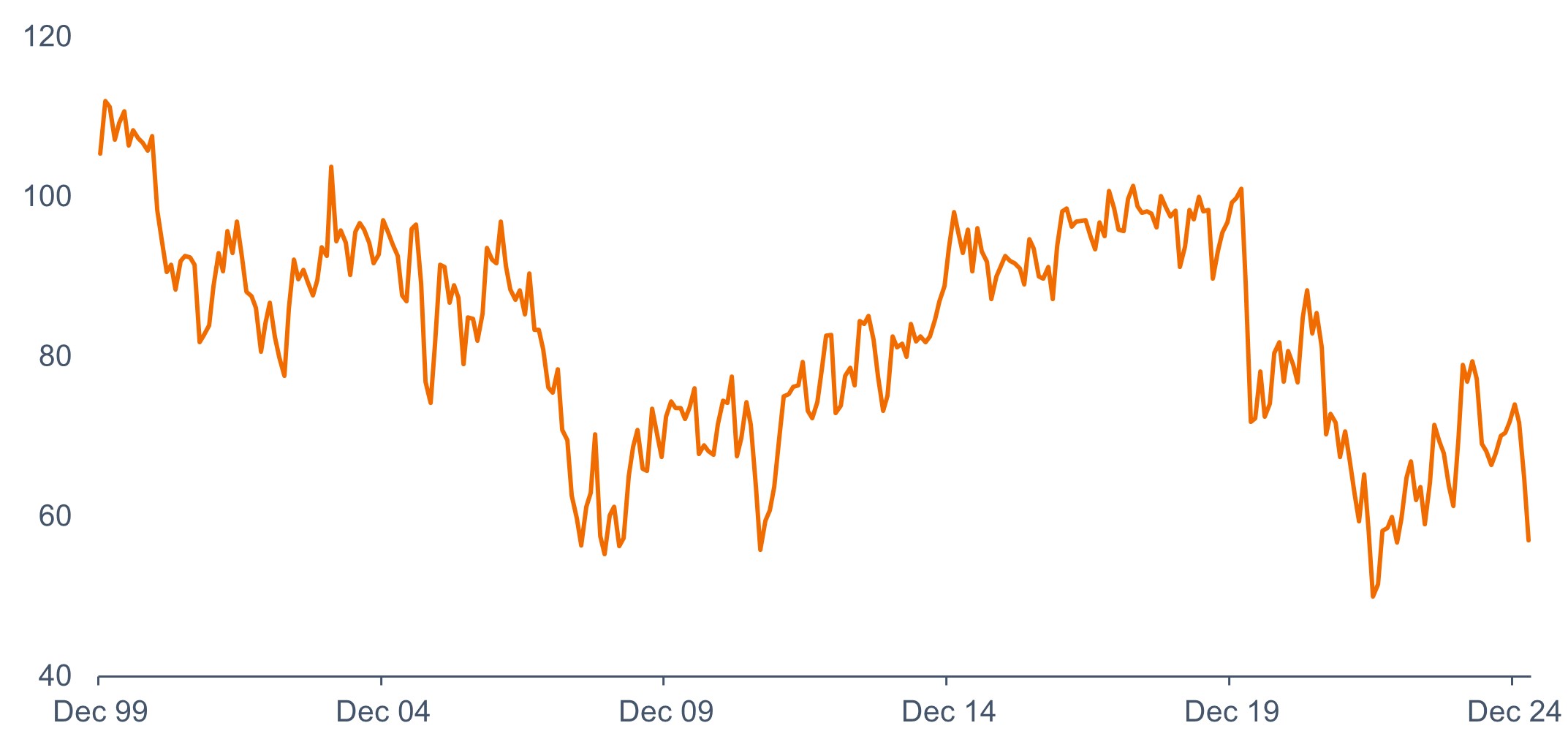

US consumers have already shown their concerns about tariffs in recent surveys. The University of Michigan Consumer Sentiment Survey suggests that American consumers expect inflation to average 5% over the next year. While this perhaps should be taken with a pinch of salt, it has also coincided with a significant drop in consumer confidence as individuals worry about higher prices on the back of tariffs.

University of Michigan Consumer Sentiment Index, 31 January 1999 – 31 March 2025

Source: Bloomberg, as of 31 March 2025.

Similarly, corporate sentiment has sagged after jumping higher over the second half of 2024. The concern inside the US is that higher prices due to tariffs weigh on real income and spending growth. Outside of the US, where goods exports tend to be more economically important, the problem is more focused on the impact on industry and the knock-on effect to the wider economy.

Market implications

Recent performance differences across markets have been noticeable. After performing well following the US election in November 2024, US equities have been the biggest losers as uncertainty has risen in 2025. American stocks have lacked the positive catalysts that have driven European and Chinese equities higher year to date as both have seen new stimulus policies from their respective governments. However, this has left both looking somewhat vulnerable – particularly Europe, where there appears to be a significant time horizon gap between the negative implications of any immediate implementation of trade tariffs and the longer-term impact of higher government spending.

While it is always difficult to judge what markets are pricing in ahead of an event, we can read into a few areas for indications. Investor surveys suggest that expectations remain to the moderate side of the more extensive possible implementations of tariffs, although expectations are now more closely aligned with rhetoric than they were back in December. This suggests that if the pronouncements are in line with the messaging, there is still room for a more negative reaction. Similarly, valuations remain elevated compared to history, suggesting that an outcome with a more problematic effect on earnings may well still lead to further downside.

However, we can also find some signs of over-pessimism that may point to the move in markets becoming extended. This is most obvious in survey results showing sentiment among US retail and professional investors has soured to an extreme extent. Such bearishness about markets is often associated with better returns going forward but also doesn’t preclude further declines. However, it is also important to note that there have been fewer signs of capitulation among institutional investors. These could yet remain a source of further selling should news flow continue to cause concerns.

Portfolio positioning considerations

Perhaps the most important question is whether a global trade war can push this late-cycle economy into a global recession. Although right now we think the answer is still “no,” US equities remain relatively expensive and therefore likely sensitive to negative surprises relating to Liberation Day or any of the upcoming important US data releases (eg, Institute for Supply Management manufacturing purchasing managers index and non-farm payrolls).

It is also worth bearing in mind that timing markets is notoriously difficult, with some of the strongest market days often coming at times of uncertainty. For investors who are able to weather this short-term volatility, stimulative policy in Europe and China has the potential to combine with forthcoming stimulative US policy (eg, taxes, deregulation) to make for a fertile medium-term environment for active investors. Staying invested with a well-balanced portfolio may therefore be the best way to weather current volatility.

IMPORTANT INFORMATION

Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments.

Foreign securities are subject to currency fluctuations, political and economic uncertainty, increased volatility and lower liquidity, all of which are magnified in emerging markets. Fixed income securities are subject to interest rate, inflation, credit and default risk. As interest rates rise, bond prices usually fall, and vice versa.

Monetary Policy refers to the policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money.

Quantitative Easing (QE) is a government monetary policy occasionally used to increase the money supply by buying government securities or other securities from the market

Volatility is the rate and extent at which the price of a portfolio, security or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. The higher the volatility the higher the risk of the investment.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.