Chart to Watch: U.S. households remain solid despite uptick in consumer debt

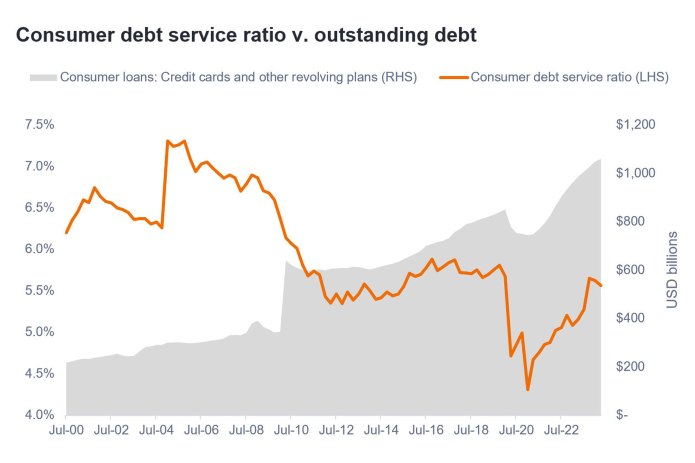

While U.S. consumer loan balances, which include credit cards and other revolving plans, recently surpassed $1 trillion for the first time in history, the rise in debt tells only half the story. U.S. households remain well capitalized, with ample ability to service consumer debt.

1 minute read

Key takeaways:

- While higher inflation has underpinned a rise in absolute debt, since 2020, U.S. households have also experienced substantial growth in the value of their assets, as well as wage and salary increases that have boosted disposable personal income.

- As a result, rising debt levels have not led to an alarming deterioration in households’ ability to service their debt. The debt service ratio has simply returned to, and stabilized around, its pre-COVID range and remains well below the concerning levels seen leading up to the Global Financial Crisis.

- In our view, the U.S. consumer – the bedrock of the U.S. economy – remains in good shape. As such, we consider the risk of recession to be low and believe investors can lean into attractive yields in securitized fixed income.

Source: Board of Governors of the U.S. Federal Reserve System, as of Q2 2024. Consumer debt service ratio = Consumer debt service payments as a percentage of disposable personal income.

The U.S. consumer is in much better shape than one might believe reading the press. While some lower-income households might be experiencing financial strain, middle- and upper-income households – which represent a much larger portion of the overall economy – have benefited from stock portfolios and home values rising to all-time highs, low levels of unemployment, and wages that continue to grow well ahead of their pre-COVID rates. As active fixed income managers, we have the ability to be selective about the types and quality of consumer credit we are exposed to and can seek to avoid concerning parts of the market.

– John Kerschner, Head of US Securitised Products

- The Chart to Watch series highlights data trends that matter. Our investment teams provide insight on what these mean for investors.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

1 minute read

Key takeaways:

- While higher inflation has underpinned a rise in absolute debt, since 2020, U.S. households have also experienced substantial growth in the value of their assets, as well as wage and salary increases that have boosted disposable personal income.

- As a result, rising debt levels have not led to an alarming deterioration in households’ ability to service their debt. The debt service ratio has simply returned to, and stabilized around, its pre-COVID range and remains well below the concerning levels seen leading up to the Global Financial Crisis.

- In our view, the U.S. consumer – the bedrock of the U.S. economy – remains in good shape. As such, we consider the risk of recession to be low and believe investors can lean into attractive yields in securitized fixed income.