COLLATERALIZED LOAN OBLIGATIONS

Understanding Collateralized Loan Obligations (CLOs)

Whether you're new to CLOs or looking to deepen your understanding, our resources help you explore how CLOs work, their market size and history, and key characteristics of the asset class.

Explore how you can access CLOs through Janus Henderson ETFs

AAA CLO ETF

For investors looking for a fund that seeks to generate yield above money markets while maintaining high-quality benefits.

BBB CLO ETF

For investors looking for a fund that aims to maximize yield in a floating rate strategy.

Securitized Income ETF

For investors looking for income diversification and higher yield potential.

What is a collateralized loan obligation?

CLOs are managed portfolios of bank loans that have been securitized into new instruments of varying credit ratings. CLOs have increasingly become the link between the financing needs of smaller companies and investors seeking higher yields.

Size and history of the CLO market

CLOs have been part of the U.S. securitized products market since the late 1980s. Historically, most CLOs were privately sold to large institutional investors such as banks, insurance companies, and asset management companies.

The CLO market has grown impressively, reaching about $1.1 trillion in assets. With over $100 billion in new issuances annually in 2023 and 2024, it's quickly approaching the size of the $1.4 trillion corporate high-yield bond market. This growth demonstrates the CLO market's emerging significance and liquidity and highlights CLOs as a compelling option for investors seeking diversification and growth.

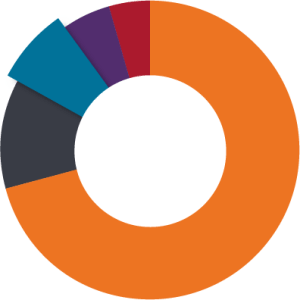

CLO makes up a $1.1T portion of the $14.6 trillion U.S. securitized market

- Agency MBS │ $9.1T

- CMBS | $1.8T

- CLOs | $1.1T

- ABS | $880B

- Non-agency RMBS | $1.7T

Source: Bank of America, as of December 31, 2024.

Six key characteristics of CLOs

1

Strong credit ratings

CLOs stand out for their robust credit quality, with approximately 80% of securities rated between AAA and A. In fact, no AAA rated CLO has ever defaulted in the asset class's 30+ year history.

2

A structure that honors credit quality

If collateral in the CLO is insufficient, cash flows for lower tranches are rerouted to higher tranches, beginning with AAA. Therefore, in times of market stress, the credit quality of the higher-rated tranches generally improves.

Over 70% of loans in a CLO must default to impair the AAA tranche. For context, the peak default rate during the Global Financial Crisis was 12%.

3

Floating interest rates

Floating-rate securities like CLOs have yields that adjust with benchmark rates, making them less sensitive to interest rate changes than most fixed-rate bonds, whose prices react inversely to rate shifts.

In the U.S., where fixed-rate bonds are more common, high-quality floating-rate options are scarce. Investors seeking floating-rate exposure often settle for lower credit-quality direct bank loans. CLOs offer an alternative, providing floating-rate exposure through investment-grade assets.

4

Attractive yields

Despite their higher credit ratings, CLOs have offered attractive yields relative to other fixed income asset classes. BBB rated CLOs tended to offer yields closer to the sub-investment grade bank loan and high-yield corporate bond markets. AAA tranches typically offered yields comparable to corporate bonds, notwithstanding their higher average credit quality.

One explanation for the higher yields is the relative newness of the market, including many investors’ lack of familiarity with CLOs.

Source: Bloomberg, JP Morgan, as of December 29, 2023. Average yield to worst: January 2021 – December 2023. Indices used to represent asset classes; BBB CLOs = J.P. Morgan CLO BBB Index, and High yield = Bloomberg U.S. Corporate High Yield Bond Index.

5

Diversification

Most benchmark indexes, such as the Bloomberg U.S. Aggregate Bond Index, the Bloomberg U.S. Corporate High Yield Index, and the Bloomberg Global Aggregate Bond Index, are comprised of 100% fixed-rate bonds. Portfolios that are exclusively allocated to these indexes are negatively correlated to changes in interest rates – their prices go down when interest rates rise.

CLOs offer diversification from many fixed income markets in that they have exhibited relatively low correlations to the major asset classes. Given their floating-rate yields, the low correlation to fixed-rate bonds is not surprising.

6

Liquidity

Liquidity risk – the risk that an investor will not be able to quickly and easily sell an asset – is a key consideration for investors.

The strong growth of the CLO market has been accompanied by increased trading volumes and improving liquidity. In March 2020, when bond market volatility was peaking and volumes in many fixed income markets fell precipitously, trading volume in CLOs surged.

Meanwhile, the number of CLO managers has grown steadily, increasing both liquidity in the secondary market and willingness on the part of broker/dealers to transact and hold the products.

Risk considerations for CLOs

CLOs are complex, and while they usually have a high credit rating, they also have inherent risks.

- The underlying loans are issued to below-investment grade corporations whose revenues and cash flows may be affected by economic shifts, potentially impairing their ability to make loan payments.

- Borrowers have the ability to pay off their loans early, making CLOs subject to prepayment risk, which could lead to lower reinvestment interest rates for investors.

Why Janus Henderson for CLOs?

Expertise and leadership: Our portfolio management team's nearly 60 years of combined experience, backed by a dedicated global team, stands as a testament to our success. This unparalleled expertise ensures we remain at the forefront of CLO investment management.

Market dominance: Janus Henderson's JAAA dominates the U.S. AAA CLO ETF market, capturing over 80% of the market's assets under management. JAAA also leads globally in inflows and ranks as the 3rd-largest active fixed-income ETF, highlighting our innovative edge and market leadership.

Source: Morningstar as of June 30, 2024.

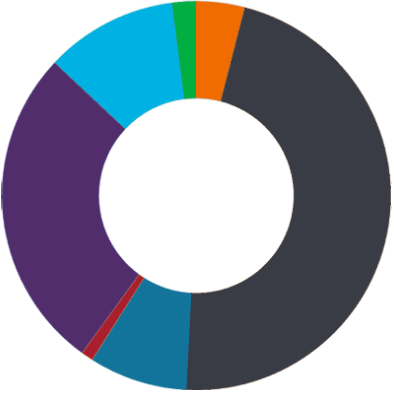

$44.6B

Firmwide Securitized assets under management

- ABS │ 4%

- CLO │ 47%

- CMBS │ 8%

- Covered Bonds │ 1%

- MBS │ 27%

- RMBS │ 11%

- Other │ 2%

Source: Janus Henderson Investors as of December 31, 2024.

Note: Firmwide assets include securitized products available outside of the U.S. and securitized portions of other fixed-income strategies.

Dedicated CLO Expertise

Global Head of Securitised Products | Portfolio Manager

Head of Structured and Quantitative Fixed Income | Portfolio Manager

Portfolio Manager | Securitised Products Analyst