A US small-cap awakening: Positive momentum for 2025

Portfolio Manager Jonathan Coleman outlines why he believes momentum in U.S. small-cap stocks can carry over into 2025, highlighting favorable macroeconomic shifts, potential policy tailwinds, and appealing relative valuations.

4 minute read

Key takeaways:

- U.S. small-cap stocks are showing renewed performance strength. We believe factors behind the shift – including broadening economic growth, moderate inflation, and easing monetary policy – have staying power for 2025.

- Relative to large caps, investors may also see an increase in small cap opportunities due to lower valuations, the potential for higher earnings growth, and benefits from domestic policy trends.

- When considering an allocation to small-cap stocks, we think investors should focus on high-quality companies with strong growth potential given the wide dispersion in fundamentals and valuations across the investable universe.

A small-cap awakening could be underway. Investor sentiment has improved for this segment of the market, driven by a shift in performance leadership and positive fundamental factors. Since July 10, the S&P SmallCap 600® Index has approximately doubled the return of the S&P 500® Index, marking a significant turning point for the asset class (Figure 1).

The recent rally in small-cap stocks followed a softer Consumer Price Index (CPI) report in early July. This allowed the Federal Reserve (Fed) to implement a 50 basis-point interest-rate cut, a move that has historically favored small-cap stocks. The momentum continued after the U.S. election, driven by optimism around the new administration’s anticipated pro-growth economic policies, which could also have positive ramifications for small caps.

We believe several factors position small caps for continued momentum in 2025, including favorable macroeconomic conditions, domestic policy tailwinds, and appealing relative valuations.

Figure 1: Two small cap rotations occurred in the second half of 2024

Source: Bloomberg, as at 11 December 2024.

Favorable macro conditions

The current environment – characterized by broadening economic growth, moderate inflation, and easing monetary policy – has supported small cap outperformance in the past.

Small caps have historically outperformed in the year following Fed rate cuts, a pattern we are witnessing again. While inflation remains above the Fed’s 2% target, further rate cuts are expected, though at a more measured pace.

Lower interest rates reduce companies’ funding costs and make long-term earnings trajectories more attractive. This is particularly significant for smaller companies, which tend to have a higher proportion of floating rate debt compared to larger firms. Additionally, lower inflation could disproportionally benefit small-cap earnings expansion due to their typically lower pricing power and higher labor intensity.

Domestic policy tailwinds

U.S. small-cap stocks stand to benefit from the ongoing deglobalization of supply chains, often called reshoring or onshoring. An increasing tariff regime creates opportunities for companies with greater exposure to the U.S. economy. Since small caps generate less revenue from outside the U.S. than their large cap peers, potential trade barriers could further enhance their attractiveness.

The incoming administration is likely to prioritize domestic growth through policies including tax cuts, targeted fiscal stimulus, and deregulation. These approaches could provide support for small-cap stocks, which are more economically sensitive than their larger counterparts. We expect small-cap earnings growth could exceed that of large-cap stocks in 2025, aided by easier earnings comparisons.

Attractive relative valuations

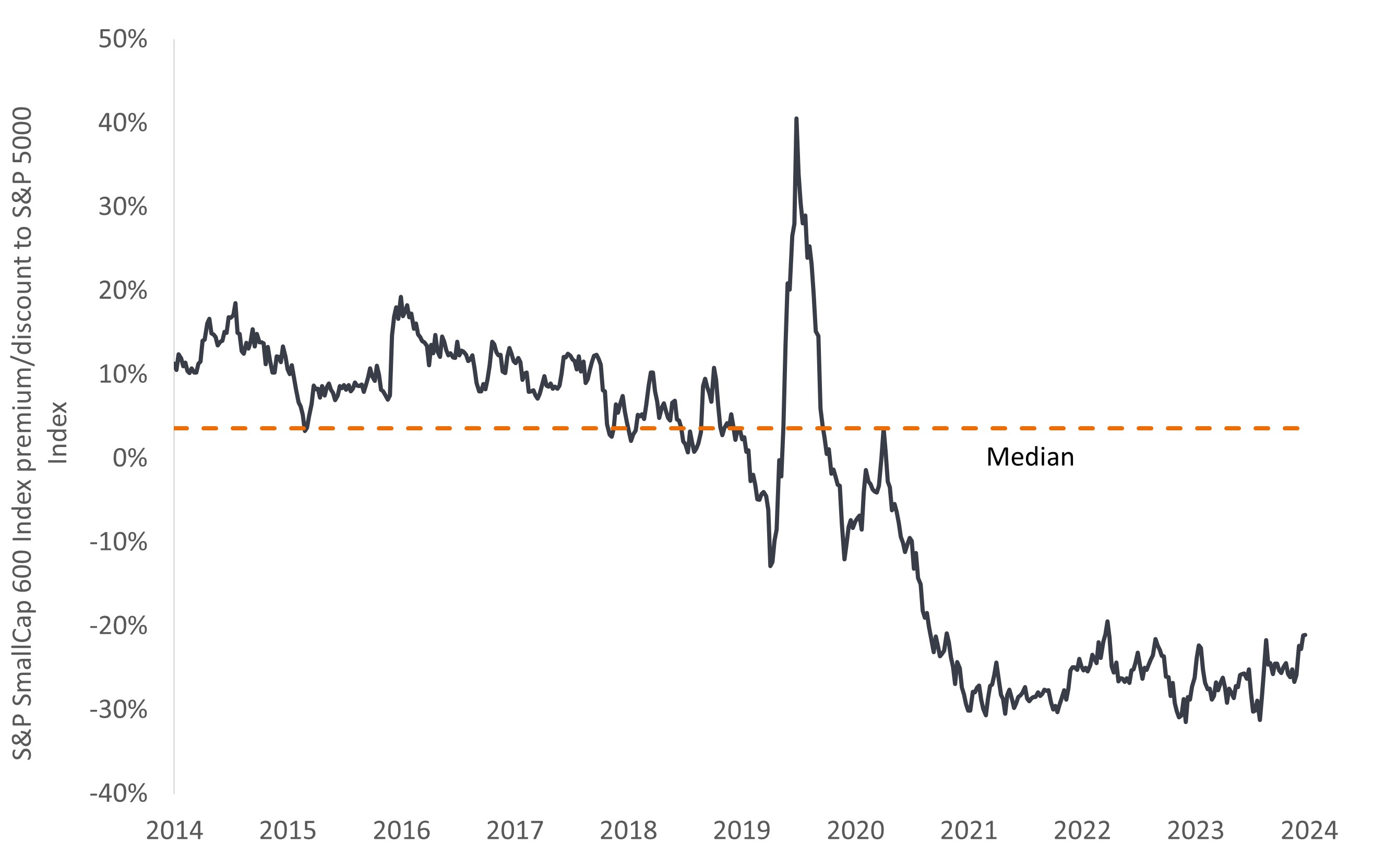

Currently, small caps are trading at a discount to large-cap stocks, offering an attractive entry point. The relative valuation on a forward price-to-earnings basis sits at a historically appealing level (Figure 2). This valuation gap, combined with potential higher earnings growth rates, makes the asset class a compelling investment opportunity.

Figure 2: Small caps are less expensive than large caps on a forward price-to-earnings basis

Relative forward P/E of the S&P SmallCap 600 Index to the S&P 500 Index

Source: Bloomberg; data reflect forward 12-month price-to-earnings (P/E) ratios. Data are weekly from 19 December 2014 to 29 November 2024.

Notably, it is important to recognize that the small- versus large-cap performance cycle operates in long cyclical patterns, with outperformance periods typically lasting between six and 14 years. We are currently in the 13th year of a large-cap outperformance cycle and potentially at the early stages of an extended small-cap outperformance cycle.

Risk considerations

While our outlook is positive overall, two underappreciated risks warrant careful consideration. First, aggressive tariff policies could create significant inflationary impacts and potentially restrain consumer spending, which drives about 70% of U.S. economic growth. While the market currently prioritizes growth potential over the risk of an inflation resurgence, the initial policy enthusiasm may moderate.

Second, potential changes from government efficiency initiatives could create headwinds for sectors previously viewed as benefiting from the status quo, such as healthcare and defense.

Navigating market complexities

We believe the current environment offers ample opportunities for active stock selection. Wide dispersion exists in valuations, quality, and growth prospects within the small-cap universe. Notably, 36% of Russell 2000 constituents remain unprofitable. By focusing on high-quality companies with strong fundamentals and growth potential, we believe investors can better capitalize on opportunities presented by this asset class.

As investors increasingly recognize the potential of this asset class, we believe small caps are well positioned to maintain positive momentum. Furthermore, the current economic and fundamental drivers combined with attractive valuations make small caps a compelling investment consideration for the year ahead.

S&P 500® Index reflects U.S. large-cap equity performance and represents broad U.S. equity market performance.

S&P SmallCap 600® Index seeks to measure the small-cap segment of the U.S. equity market. The index is designed to track companies that meet specific inclusion criteria to ensure that they are liquid and financially viable.

Consumer Price Index (CPI) is an unmanaged index representing the rate of inflation of the U.S. consumer prices as determined by the U.S. Department of Labor Statistics.

Basis point (bp) equals 1/100 of a percentage point. 1 bp = 0.01%, 100 bps = 1%.

Monetary Policy refers to the policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money.

Price-to-Earnings (P/E) Ratio measures share price compared to earnings per share for a stock or stocks in a portfolio.

Russell 2000® Index reflects the performance of U.S. small-cap equities.

Quantitative Easing (QE) is a government monetary policy occasionally used to increase the money supply by buying government securities or other securities from the market.

Smaller capitalization securities may be less stable and more susceptible to adverse developments, and may be more volatile and less liquid than larger capitalization securities.

All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information.

4 minute read

Key takeaways:

- U.S. small-cap stocks are showing renewed performance strength. We believe factors behind the shift – including broadening economic growth, moderate inflation, and easing monetary policy – have staying power for 2025.

- Relative to large caps, investors may also see an increase in small cap opportunities due to lower valuations, the potential for higher earnings growth, and benefits from domestic policy trends.

- When considering an allocation to small-cap stocks, we think investors should focus on high-quality companies with strong growth potential given the wide dispersion in fundamentals and valuations across the investable universe.