Key takeaways:

- Fundamental changes in global geopolitical relations are causing heightened market volatility.

- Markets are now pricing our long-held view of 100bps easing by the RBA this cycle.

- We remain modestly long duration, favouring the short to mid part of the curve.

- Monthly focus: The fiscal outlook has deteriorated, as expected, but Australia remains comparatively prudent.

Market review

It has been a particularly volatile month as markets absorb the fundamental changes in global geopolitical relations. Erosion of multi-decade beneficial global trade policy, deterioration of geopolitical relations, and a broad re-focusing on political rather than economic outcomes, is causing markets to question the potential economic growth and inflation outcomes ahead. The Australian bond market, as measured by the Bloomberg AusBond Composite 0+ Yr Index, rose 0.17%.

The Reserve Bank of Australia (RBA) is on its new six weekly cycle and did not meet in March, with the cash rate remaining at 4.10%. Three-month bank bills were up 1 basis point (bp), to 4.13%. Six-month bank bill yields ended 8bps higher at 4.30%. Australia’s three-year government bond yields ended the month 4bps lower, at 3.70%, while 10-year government bond yields were 9bps higher at 4.38%. The divergence highlights the differing forces over the tenors, with the three-year dominated by RBA pricing, and the 10-year buffeted by rising global geopolitical risks which point to possibly stagflationary outcomes. This divergence was expected and accounted for in our long duration position.

Financial markets are watching the evolution of the Trump Government’s policies, applying probable implications to prices as the information changes. Markets have been particularly volatile, with equities leading the moves but bond markets are also responding. To date, US trade, immigration, fiscal and regulatory policies have yet to be fully implemented, and the policy outcomes remain unclear, for the US but also the rest of the world. Changes in German fiscal and defence policy are impactful, changing the growth and spending trajectory in the region. This drove significant increases in longer dated German and Japanese yields.

The Australian economy continued its sluggish path, with fourth quarter GDP rounding the year at a modest 1.3% year on year (yoy). There were modest signs of improvement from the household sector, while the government sector drove a substantial amount of growth. Monthly inflation moderated fractionally, to 2.4% yoy, while employment dropped sharply in February. The unemployment rate remained at 4.1%, due to an unusual fall in the participation rate. The RBA will look through all the noise, but the moderation should provide marginal comfort that they have room to lower the cash rate. The 2025-26 Federal Budget was released and, while expansionary, was in line with expectations. We now see GDP growth rising 2.5% in the 2025 year if the household is provided relief.

Market outlook

Markets are likely to continue to be buffeted by global squalls amid policy uncertainty and crosscurrents. The domestic market, having seen the RBA commence easing, is likely beholden to the inflation outlook, but also cognisant of the global ructions’ potential to alter the growth outlook. Our base case is for the RBA to proceed with a modest easing cycle, of around 100bps in total to 3.35%, spread across 2025. With global uncertainty, we have no active bias; our high case is one in which the domestic economy rebounds quickly and the RBA only ease twice for a total of 50bps. The low case is for more easing over the whole cycle. The market is pricing for a low in the cash rate of 3.31%, similar to our central scenario. We maintain a modest overweight duration position and look to adjust the position as volatility brings opportunity for market mispricing. We continue to favour the shorter part of the yield curve, as the long end is caught up with global factors.

Monthly focus – How much is too much fiscal spending

Fiscal deficits and higher government debt levels are now the norm, and it appears they are only going to get bigger. In an aging society, post the global pandemic, rising health care spending is entrenched and socially expected. A changing global landscape points to a rising in defence spending not seen since the second world war, with Germany and Japan even loosening their defence spending rules. In this context, it was always expected that Australia re-join the net spending club.

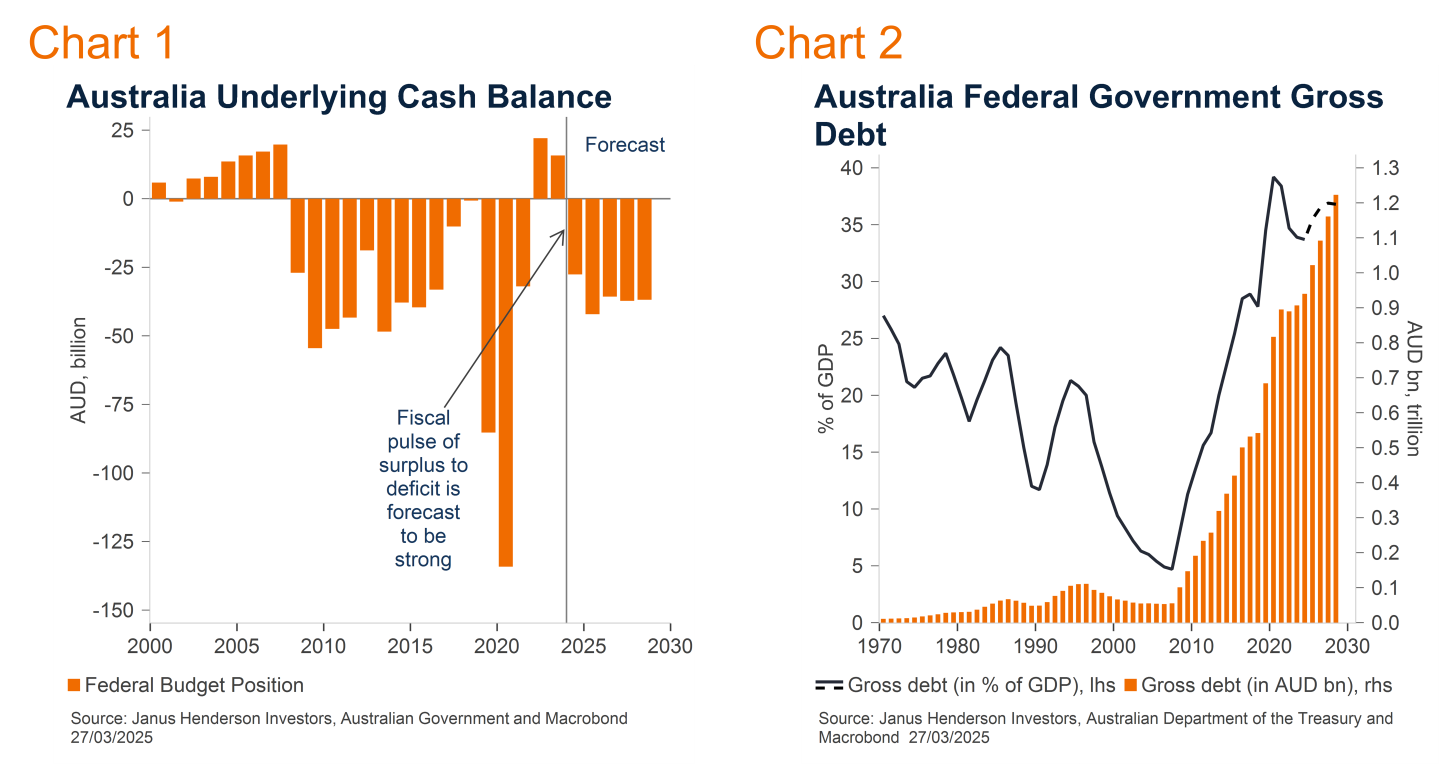

Ahead of the upcoming election, the incumbent Government released a Budget that was mostly in-line with previously flagged fiscal expansion. The Government headline cash balance moves from an upwardly revised surplus of $15.8bn in 2023-24 to a deficit of $27.6bn in the 2024-25 year, and it expands in the following year (Chart 1). This sees the government spending contribution to GDP remaining robust in 2025, after a strong contribution in 2024.

It was this government spending that offset subdued household and private investment sectors, preventing a recession in 2024. The growth outlook for 2025 looks better than the pallid 1.3% year on year GDP 2024 outcome, but remains partially reliant on a full spending government sector for trend growth.

The RBA has had reservations about the extent of the fiscal pulse in early 2025, which has resulted in some caution on the path for monetary policy. The published Budget may have alleviated concerns of even greater fiscal firepower preventing any further easing of monetary policy. The deficit numbers are large, but they do not suggest a change in our expected RBA easing path.

The projected deficits, adding to the existing level of debt, leaves Australia’s gross debt at high, and rising levels. By 2028, Australia’s Federal gross debt is forecast to reach 37% of GDP, below the Covid peak, but still significant (Chart 2). However, by global standards, gross debt is comparatively modest. It is for this reason that Australia still enjoys its AAA rating, when a number of our G10 peers no longer do.

Global investors, when comparing Australia’s government debt to that of other countries, use a measure which adds the state government debt to that of the Federal Government. On this measure, and using the International Monetary Fund debt database, ensuring equal comparisons, Australia still registers as having a relatively low level of Government debt to GDP, at 50%. This remains well below the US at 120%, and even Germany at 65%.

Longer term, failure to repair growing debt levels will be a global problem, one which started as Governments did not address debt levels post the Global Financial Crisis in 2008 and then escalated in the Covid-19 Pandemic. This can continues to be kicked down the road, but for now, there are greater issues to be addressed, and markets should remain relatively comfortable with Australia’s debt levels.

Views as at 1 April 2025.

All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information.