Euro-IG-Unternehmensanleihen: Eine Geschichte von Spreads und Renditen

European investment grade (IG) corporate bonds still offer investors the potential to enjoy an attractive income and future total return, according to Client Portfolio Manager Celia Soares and Portfolio Manager Tim Winstone. For active investors, considerable dispersion in the market adds to the upside appeal.

4 Minuten Lesezeit

Zentrale Erkenntnisse:

- Yields per unit of spread have trended lower for much of the past 15 years, reflecting a post Global Financial Crisis (GFC) period of accommodative central bank intervention, structurally low yields, high investor demand and low spreads. Typically, investors searching for an attractive yield in this environment needed to add risk by decreasing credit quality or extending duration.

- More recently, we have seen the yield-to-risk ratio for Euro investment grade corporates begin to improve and we expect this normalisation to continue. If corporate yields follow sovereign yields downward from recent highs, corporate spreads could stabilise or move slightly lower.

- Downside risks to spreads do exist (eg. rate volatility and a challenging economic backdrop in Europe). However, attractive all-in yields right now – as well as offering investors the potential for an attractive income and future total return – should serve as a buffer against possible volatility and spread widening.

2023 was a year of ups and downs for the Euro area. It started with surprising resilience to an energy crisis and the return of war to the continent but towards the second half of the year it was clear that the impact of monetary tightening, weaker global growth and high gas prices would have a lagged impact on European growth. This proved to be a challenge for European investment grade (IG) corporates, which saw their performance fall behind that of their counterparts in the United States.

Investors viewed this divergence of spreads as a potential opportunity and, as a result, European IG corporates have been recouping some of their relative underperformance. However, investors are now questioning if there is any value left in the current spreads due to the ongoing challenging economic backdrop and risks on the downside.

When attempting to answer this question, many analysts view the most recent 10-year average as representative sample and compare it to current spread levels. This, however, besides indicating some time-anchoring bias, reflects a time of suppressed yields, high investor demand and low spreads.

JHI

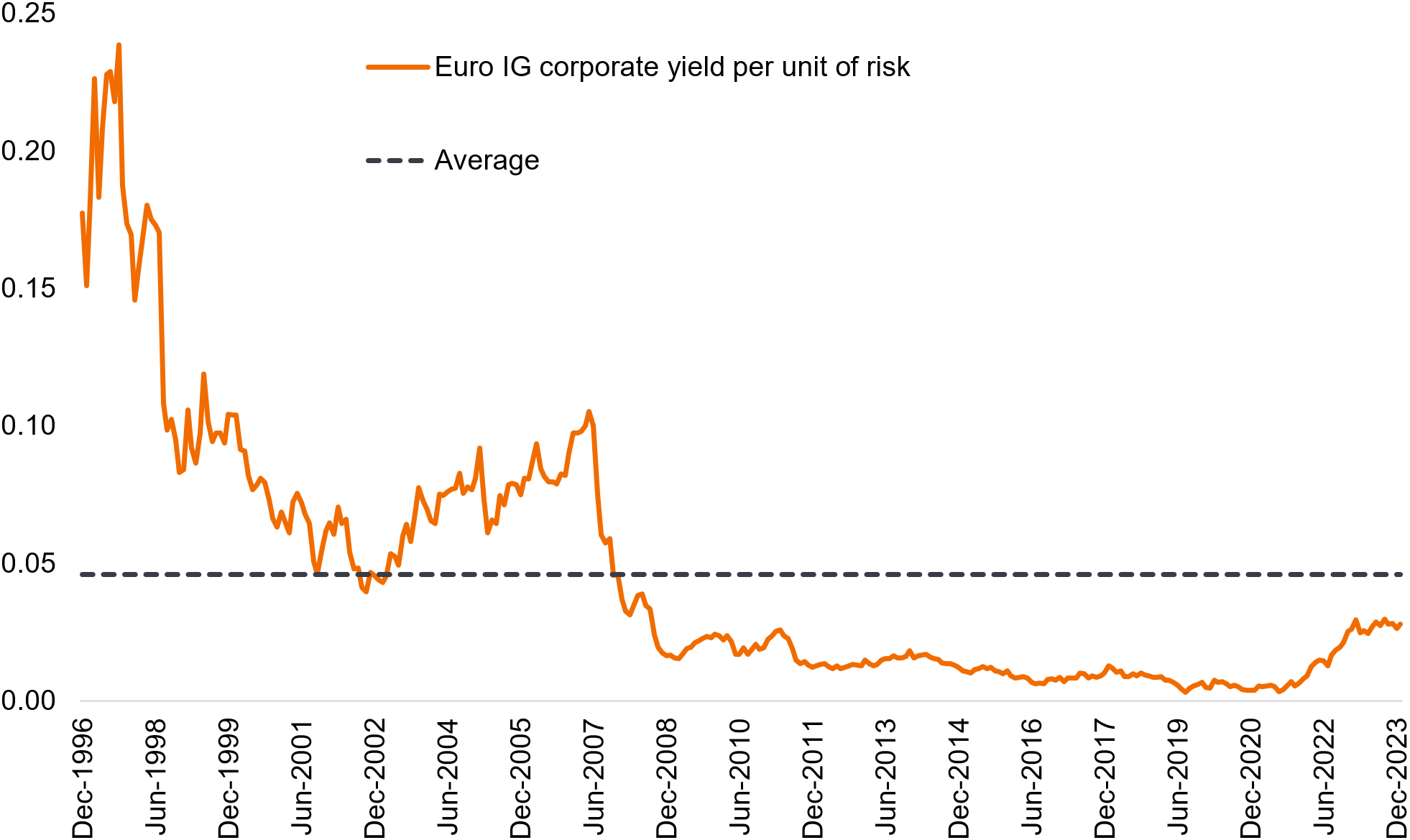

As shown in Figure 1, the yield investors receive per unit of spread has been on a downward trend since the Global Financial Crisis (GFC), and only recently has it started to tick upwards back to its long-term average. In order to add the same yield, post-GFC investors had to add more risk to their portfolios by decreasing credit quality or extending maturity.

Figure 1: Euro IG yield per unit of risk: a long-term perspective

Yield per unit of risk has been on a downward trend since the Global Financial Crisis

Source: Janus Henderson, Bloomberg 2024 (ICE Bofa Euro Corporate Index). Data from 31 December 1996 to 31 January 2024. Past performance does not predict future returns.

But are Euro IG corporate markets post-GFC intrinsically different? The last decade was marked by strong central bank intervention which kept yields structurally low, but with recent inflationary pressures and rapid central market intervention, we are perhaps turning the corner on ultra-low yields. As a result, we should expect the yield-to-risk ratio to continue to normalise, which means that if IG corporate yields follow sovereign yields’ downward trend (from recent highs), we could see IG spreads stabilising at these levels, or moving slightly lower.

We are, however, not complacent to the downside risks of spreads and how rates volatility can impact spread returns. But we also see the opportunity these current yields offer, as they can provide a substantial buffer to total returns during periods of volatility and/or spread widening.

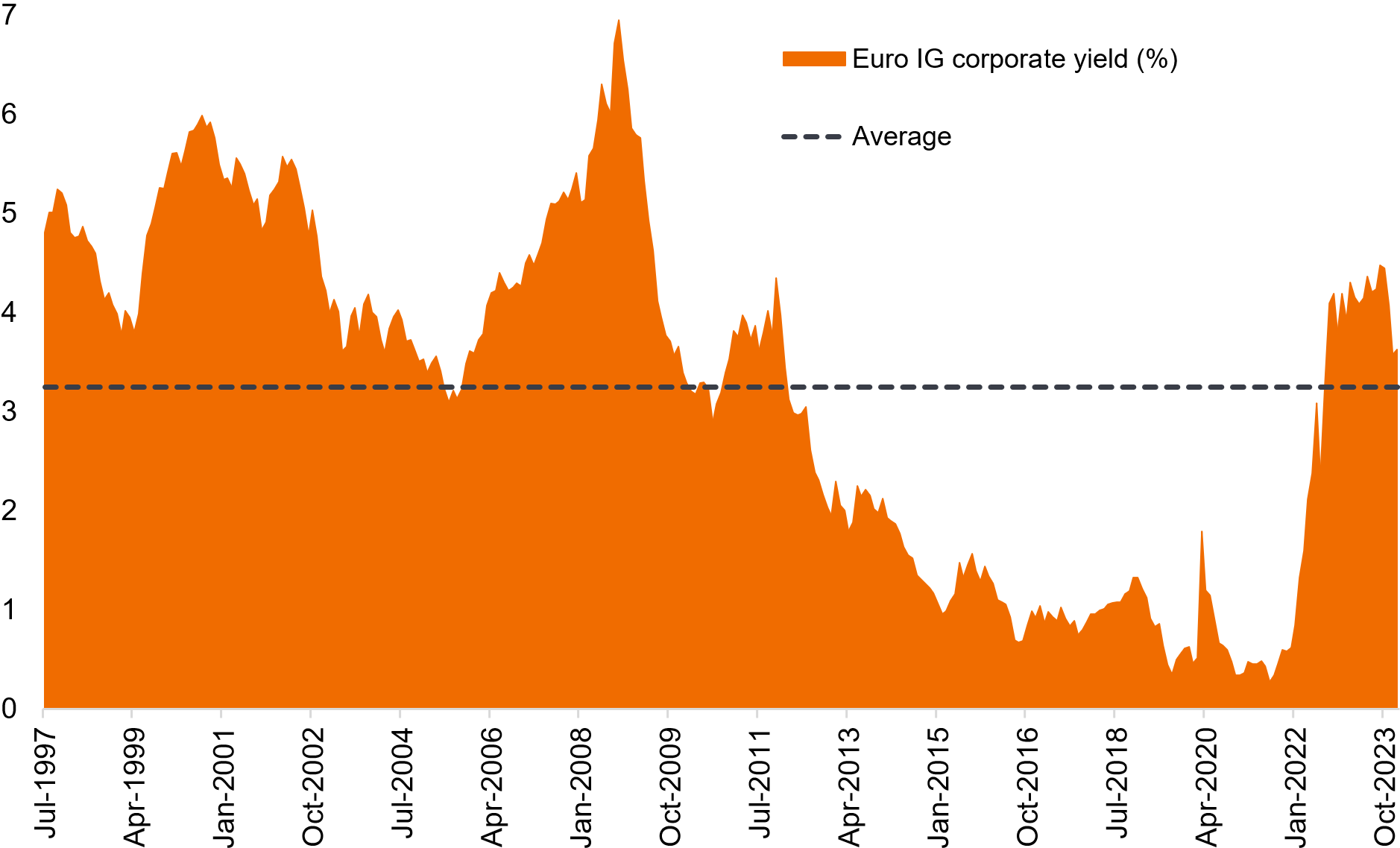

Figure 2: Euro IG yields remain attractive in a historical context

Source: Janus Henderson and Bloomberg (ICE Bofa Euro corporate). Data from 31 July 1997 to 31 January 2024. Past performance does not predict future returns.

The yields available in the European IG market still offer potential for attractive future returns and an appealing income. There is also considerable dispersion in the market, which should provide a fertile hunting ground for active investors.

Active investing. An investment management approach where a fund manager actively aims to outperform or beat a specific index or benchmark through research, analysis and the investment choices they make. The opposite of Passive Investing.

Bond. A debt security issued by a company or a government, used as a way of raising money. The investor buying the bond is effectively lending money to the issuer of the bond. Bonds offer a return to investors in the form of fixed periodic payments (a ‘coupon’), and the eventual return at maturity of the original amount invested – the par value. Because of their fixed periodic interest payments, they are also often called fixed income instruments.

Bond yield. The level of income on a security expressed as a percentage rate. For a bond, this is calculated as the coupon payment divided by the current bond price. There is an inverse relationship between bond yields and bond prices. Lower bond yields mean higher bond prices, and vice versa.

Corporate bond. A bond issued by a company. Bonds offer a return to investors in the form of periodic payments and the eventual return of the original money invested at issue on the maturity date.

Credit rating / credit quality. An independent assessment of the creditworthiness (credit quality) of a borrower by a recognised agency such as Standard & Poors, Moody’s or Fitch. Standardised scores such as ‘AAA’ (a high credit rating) or ‘B’ (a low credit rating) are used, although other agencies may present their ratings in different formats.

Kredit-Spread. Der Renditeunterschied zwischen einer Unternehmensanleihe und einem Benchmark Zinssatz (z. B. Rendite einer Staatsanleihe). Er gibt einen Hinweis auf das zusätzliche Risiko, das Kreditgeber eingehen, wenn sie Unternehmensanleihen im Vergleich zu Staatsanleihen mit gleicher Laufzeit kaufen. Eine Ausweitung der Spreads deutet im Allgemeinen auf eine Verschlechterung der Kreditwürdigkeit von Unternehmenskreditnehmern hin, während eine Verengung auf eine Verbesserung hindeutet.

Dispersion. A measure for the statistical distribution of given data. There are several methods to measure dispersion, also sometimes referred to as “scatter” or “variability”.

ICE Bofa Euro Corporate Index. The ICE BofA Euro Corporate Index tracks the performance of EUR denominated investment grade corporate debt publicly issued in the eurobond or Euro member domestic markets.

Investment grade (IG). A bond typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments, reflected in the higher rating given to them by credit ratings agencies.

Geldpolitik. Die Politik einer Zentralbank, die darauf abzielt, die Höhe der Inflation und des Wachstums einer Volkswirtschaft zu beeinflussen. Dazu gehört die Kontrolle der Zinssätze und der Geldmenge. Unter monetären Anreizen versteht man, dass eine Zentralbank die Geldmenge erhöht und die Kreditkosten senkt. Unter geldpolitischer Straffung versteht man Maßnahmen der Zentralbanken, die darauf abzielen, die Inflation einzudämmen und das Wirtschaftswachstum durch Erhöhung der Zinssätze und Reduzierung der Geldmenge zu bremsen.

WICHTIGE INFORMATIONEN

Die Volatilität misst das Risiko anhand der Streuung der Renditen für eine bestimmte Anlage.

Der Credit Spread ist der Renditeunterschied zwischen Wertpapieren mit ähnlicher Laufzeit, aber unterschiedlicher Bonität. Eine Ausweitung der Spreads deutet im Allgemeinen auf eine Verschlechterung der Kreditwürdigkeit von Unternehmenskreditnehmern hin, eine Verengung auf eine Verbesserung.

Eventuelle Swaps werden auf der Grundlage des fiktiven Risikos gemeldet.

Es gibt keine Garantie dafür, dass sich vergangene Trends fortsetzen oder prognostizierte Entwicklungen eintreten.

Festverzinsliche Wertpapiere unterliegen dem Zins-, Inflations-, Kredit- und Ausfallrisiko. Der Anleihenmarkt ist volatil. Wenn die Zinsen steigen, fallen die Anleihepreise normalerweise und umgekehrt. Die Rückzahlung des Kapitals ist nicht garantiert und die Preise können fallen, wenn ein Emittent seine Zahlungen nicht pünktlich leistet und sich seine Bonität verschlechtert.

Hochzinsanleihen oder „Junk“-Anleihen bergen ein höheres Ausfallrisiko und Preisvolatilität und können plötzliche und starke Preisschwankungen erfahren.

Beta misst die Volatilität eines Wertpapiers oder Portfolios im Verhältnis zu einem Index. Weniger als eins bedeutet eine geringere Volatilität als der Index; mehr als eins bedeutet größere Volatilität.

4 Minuten Lesezeit

Zentrale Erkenntnisse:

- Yields per unit of spread have trended lower for much of the past 15 years, reflecting a post Global Financial Crisis (GFC) period of accommodative central bank intervention, structurally low yields, high investor demand and low spreads. Typically, investors searching for an attractive yield in this environment needed to add risk by decreasing credit quality or extending duration.

- More recently, we have seen the yield-to-risk ratio for Euro investment grade corporates begin to improve and we expect this normalisation to continue. If corporate yields follow sovereign yields downward from recent highs, corporate spreads could stabilise or move slightly lower.

- Downside risks to spreads do exist (eg. rate volatility and a challenging economic backdrop in Europe). However, attractive all-in yields right now – as well as offering investors the potential for an attractive income and future total return – should serve as a buffer against possible volatility and spread widening.

2023 was a year of ups and downs for the Euro area. It started with surprising resilience to an energy crisis and the return of war to the continent but towards the second half of the year it was clear that the impact of monetary tightening, weaker global growth and high gas prices would have a lagged impact on European growth. This proved to be a challenge for European investment grade (IG) corporates, which saw their performance fall behind that of their counterparts in the United States.

Investors viewed this divergence of spreads as a potential opportunity and, as a result, European IG corporates have been recouping some of their relative underperformance. However, investors are now questioning if there is any value left in the current spreads due to the ongoing challenging economic backdrop and risks on the downside.

When attempting to answer this question, many analysts view the most recent 10-year average as representative sample and compare it to current spread levels. This, however, besides indicating some time-anchoring bias, reflects a time of suppressed yields, high investor demand and low spreads.

JHI

As shown in Figure 1, the yield investors receive per unit of spread has been on a downward trend since the Global Financial Crisis (GFC), and only recently has it started to tick upwards back to its long-term average. In order to add the same yield, post-GFC investors had to add more risk to their portfolios by decreasing credit quality or extending maturity.

Figure 1: Euro IG yield per unit of risk: a long-term perspective

Yield per unit of risk has been on a downward trend since the Global Financial Crisis

Source: Janus Henderson, Bloomberg 2024 (ICE Bofa Euro Corporate Index). Data from 31 December 1996 to 31 January 2024. Past performance does not predict future returns.

But are Euro IG corporate markets post-GFC intrinsically different? The last decade was marked by strong central bank intervention which kept yields structurally low, but with recent inflationary pressures and rapid central market intervention, we are perhaps turning the corner on ultra-low yields. As a result, we should expect the yield-to-risk ratio to continue to normalise, which means that if IG corporate yields follow sovereign yields’ downward trend (from recent highs), we could see IG spreads stabilising at these levels, or moving slightly lower.

We are, however, not complacent to the downside risks of spreads and how rates volatility can impact spread returns. But we also see the opportunity these current yields offer, as they can provide a substantial buffer to total returns during periods of volatility and/or spread widening.

Figure 2: Euro IG yields remain attractive in a historical context

Source: Janus Henderson and Bloomberg (ICE Bofa Euro corporate). Data from 31 July 1997 to 31 January 2024. Past performance does not predict future returns.

The yields available in the European IG market still offer potential for attractive future returns and an appealing income. There is also considerable dispersion in the market, which should provide a fertile hunting ground for active investors.

Active investing. An investment management approach where a fund manager actively aims to outperform or beat a specific index or benchmark through research, analysis and the investment choices they make. The opposite of Passive Investing.

Bond. A debt security issued by a company or a government, used as a way of raising money. The investor buying the bond is effectively lending money to the issuer of the bond. Bonds offer a return to investors in the form of fixed periodic payments (a ‘coupon’), and the eventual return at maturity of the original amount invested – the par value. Because of their fixed periodic interest payments, they are also often called fixed income instruments.

Bond yield. The level of income on a security expressed as a percentage rate. For a bond, this is calculated as the coupon payment divided by the current bond price. There is an inverse relationship between bond yields and bond prices. Lower bond yields mean higher bond prices, and vice versa.

Corporate bond. A bond issued by a company. Bonds offer a return to investors in the form of periodic payments and the eventual return of the original money invested at issue on the maturity date.

Credit rating / credit quality. An independent assessment of the creditworthiness (credit quality) of a borrower by a recognised agency such as Standard & Poors, Moody’s or Fitch. Standardised scores such as ‘AAA’ (a high credit rating) or ‘B’ (a low credit rating) are used, although other agencies may present their ratings in different formats.

Kredit-Spread. Der Renditeunterschied zwischen einer Unternehmensanleihe und einem Benchmark Zinssatz (z. B. Rendite einer Staatsanleihe). Er gibt einen Hinweis auf das zusätzliche Risiko, das Kreditgeber eingehen, wenn sie Unternehmensanleihen im Vergleich zu Staatsanleihen mit gleicher Laufzeit kaufen. Eine Ausweitung der Spreads deutet im Allgemeinen auf eine Verschlechterung der Kreditwürdigkeit von Unternehmenskreditnehmern hin, während eine Verengung auf eine Verbesserung hindeutet.

Dispersion. A measure for the statistical distribution of given data. There are several methods to measure dispersion, also sometimes referred to as “scatter” or “variability”.

ICE Bofa Euro Corporate Index. The ICE BofA Euro Corporate Index tracks the performance of EUR denominated investment grade corporate debt publicly issued in the eurobond or Euro member domestic markets.

Investment grade (IG). A bond typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments, reflected in the higher rating given to them by credit ratings agencies.

Geldpolitik. Die Politik einer Zentralbank, die darauf abzielt, die Höhe der Inflation und des Wachstums einer Volkswirtschaft zu beeinflussen. Dazu gehört die Kontrolle der Zinssätze und der Geldmenge. Unter monetären Anreizen versteht man, dass eine Zentralbank die Geldmenge erhöht und die Kreditkosten senkt. Unter geldpolitischer Straffung versteht man Maßnahmen der Zentralbanken, die darauf abzielen, die Inflation einzudämmen und das Wirtschaftswachstum durch Erhöhung der Zinssätze und Reduzierung der Geldmenge zu bremsen.

WICHTIGE INFORMATIONEN

Die Volatilität misst das Risiko anhand der Streuung der Renditen für eine bestimmte Anlage.

Der Credit Spread ist der Renditeunterschied zwischen Wertpapieren mit ähnlicher Laufzeit, aber unterschiedlicher Bonität. Eine Ausweitung der Spreads deutet im Allgemeinen auf eine Verschlechterung der Kreditwürdigkeit von Unternehmenskreditnehmern hin, eine Verengung auf eine Verbesserung.

Eventuelle Swaps werden auf der Grundlage des fiktiven Risikos gemeldet.

Es gibt keine Garantie dafür, dass sich vergangene Trends fortsetzen oder prognostizierte Entwicklungen eintreten.

Festverzinsliche Wertpapiere unterliegen dem Zins-, Inflations-, Kredit- und Ausfallrisiko. Der Anleihenmarkt ist volatil. Wenn die Zinsen steigen, fallen die Anleihepreise normalerweise und umgekehrt. Die Rückzahlung des Kapitals ist nicht garantiert und die Preise können fallen, wenn ein Emittent seine Zahlungen nicht pünktlich leistet und sich seine Bonität verschlechtert.

Hochzinsanleihen oder „Junk“-Anleihen bergen ein höheres Ausfallrisiko und Preisvolatilität und können plötzliche und starke Preisschwankungen erfahren.

Beta misst die Volatilität eines Wertpapiers oder Portfolios im Verhältnis zu einem Index. Weniger als eins bedeutet eine geringere Volatilität als der Index; mehr als eins bedeutet größere Volatilität.