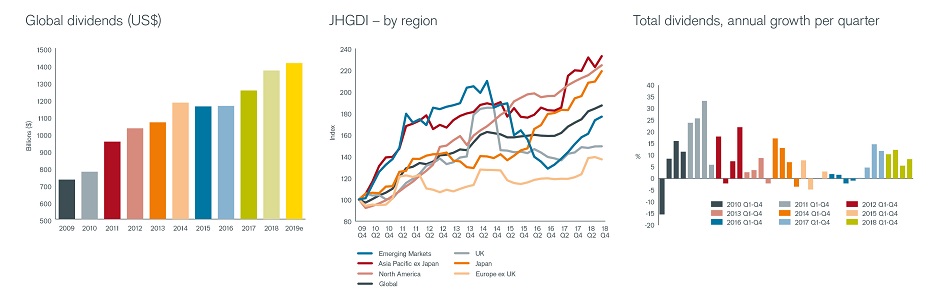

- Global dividends rose 9.3% to a record $1.37 trillion, equivalent to core underlying growth of 8.5%, the best performance since 2015

- Nine in ten companies globally increased dividends or held them flat

- Thirteen countries delivered record payouts, including Japan, the US, Canada, Germany and Russia

- Emerging markets, North America and Japan performed strongest, while Europe lagged behind

- Banking and mining payouts rose strongly, while telecoms saw the weakest performance

- Janus Henderson forecasts 2019 dividends 3.3% higher at 1.414 trillion, equivalent to underlying growth of 5.1%

Global dividends rose to a new record in 2018, with a strong fourth quarter for dividend payments despite more challenging equity market conditions, according to the latest Janus Henderson Global Dividend Index. Total dividends jumped 9.3% in headline terms to $1.37 trillion. On an underlying basis, Janus Henderson’s preferred measure of core growth, this was equivalent to an increase of 8.5%, the best performance since 2015, and above the long-term trend of 5-7%. Almost nine in ten companies around the world raised their payouts or held them steady.

Emerging markets, Japan and North America performed strongly, while Europe lagged behind. Thirteen countries delivered record payouts, including Japan, the US, Canada, Germany and Russia.

In Q4, headline dividend growth was 8.3%, yielding a total $272.9bn, a record for the fourth quarter. Underlying growth was 8.0%. The Janus Henderson Global Dividend Index ended the year at a new record 187.3, meaning the world’s companies paid their shareholders a staggering $638bn more in 2018 than 2009, when the index started.

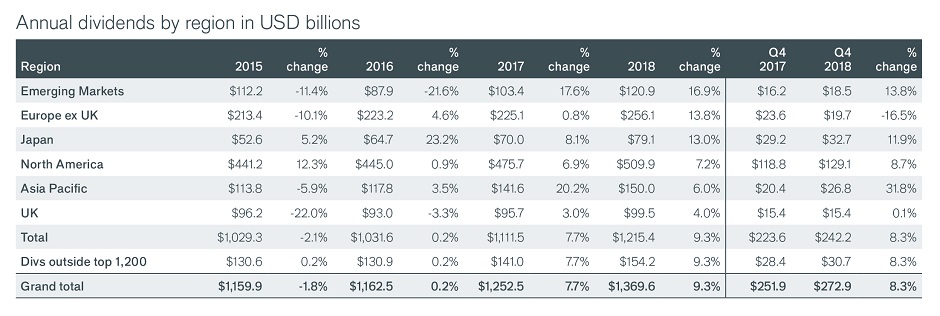

Record US dividends of $468.9bn were 7.8% higher on an underlying basis in 2018, boosted by banks, healthcare and technology companies. Only one in 25 US companies cut its payout. Canada was even stronger, thanks in particular to oil companies and banks, and enjoyed the fastest dividend growth amongst the large, developed economies. Japan saw the second fastest growth, thanks to higher company profits and rising payout ratios.

European dividends rose more slowly, up 5.4% on an underlying basis. They were held back by slow growth in Switzerland and a big cut from Anheuser Busch in Belgium. It was not a bad year, however, as nine tenths of European companies increased their dividends. Germany’s strong performance stood out, and France, Spain and Italy also did well. Headline growth benefited strongly from positive exchange-rate effects earlier in the year.

In Asia, Australia was the real weak spot in 2018. Australian dividends are heavily dependent on banks, with already high payout ratios and slow-growing profits, while the telecom operator Telstra cut its distributions sharply in a bid to preserve cash. Australian dividends rose just 0.9% year-on-year. Other countries in the region performed much better, and in South Korea, Samsung entered the global top 20 payers for the first time. Four years ago, it was not even in the top 100.

After a weak first quarter, emerging market dividends bounced back strongly over the rest of the year. For the whole of 2018, they jumped 15.9% in underlying terms. Russia contributed most to growth and saw record payouts. Chinese dividends rose strongly too.

Globally, the mining sector showed the fastest growth in 2018 as companies restored payouts boosting the UK in particular where many of them are listed. Banking dividends, the largest dividend-paying sector, jumped 13.6% on an underlying basis, while oil company distributions surged 15.4%. The telecoms sector stood out as the weakest, with payouts flat or down in half the countries in our index.

Janus Henderson forecasts underlying growth of 5.1% in 2019, which translates into headline growth of 3.3%, on the assumption that prevailing exchange rates persist all year. That means the world’s companies are set to pay their shareholders $1.414 trillion this year.

Ben Lofthouse, head of global equity income at Janus Henderson said: “Despite more challenging equity market conditions, investors can take comfort in the ability of the world’s companies to continue to generate income. Yields in many parts of the world are very attractive, while 8.5% dividend growth is ahead of the long-term trend. This strength reflects a number of factors; several sectors, such as mining, oil and banking have been normalising their dividend payments, after a period of low or no dividends, while some of the biggest tech firms are increasingly adopting a dividend-paying culture. The impact of tax cuts in the US clearly helped dividend growth there too.

For the year ahead, we expect dividend growth to be more in line with the longer-run trend. Corporate profit expectations have fallen as global economic forecasts have been revised down, although most observers still expect companies to deliver positive earnings growth in 2019. Dividends in any case are much less volatile than earnings, so we remain optimistic on the prospects for income investors.”

-ends-

Past performance is no guarantee of future results. International investing involves certain risks and increased volatility not associated with investing solely in the UK. These risks included currency fluctuations, economic or financial instability, lack of timely or reliable financial information or unfavourable political or legal developments.

Press Enquiries

Janus Henderson Investors

Lucy Forgan

T: 44 (0)207 818 2074

E: Lucy.forgan@janushenderson.com

Notes to editors

Methodology

Each year Janus Henderson analyses dividends paid by the 1,200 largest firms by market capitalisation (as at 31/12 before the start of each year). Dividends are included in the model on the date they are paid. Dividends are calculated gross, using the share count prevailing on the pay-date (this is an approximation because companies in practice fix the exchange rate a little before the pay date), and converted to USD using the prevailing exchange rate. Where a scrip dividend is offered, investors are assumed to opt 100% for cash. This will slightly overstate the cash paid out, but we believe this is the most proactive approach to treat scrip dividends. In most markets it makes no material difference, though in some, a particularly European market, the effect is greater. Spain is a particular case in point. The model takes no account of free floats since it is aiming to capture the dividend paying capacity of the world’s largest listed companies, without regard for their shareholder base. We have estimated dividends for stocks outside the top 1,200 using the average value of these payments compared to the large cap dividends over the five-year period (sourced from quoted yield data). This means they are estimated at a fixed proportion of 12.7% of total global dividends from the top 1,200, and therefore in our model grow at the same rate. This means we do not need to make unsubstantiated assumptions about the rate of growth of these smaller company dividends. All raw data was provided by Exchange Data International with analysis conducted by Janus Henderson Investors.

About Janus Henderson

Janus Henderson Group (JHG) is a leading global active asset manager dedicated to helping investors achieve long-term financial goals through a broad range of investment solutions, including equities, fixed income, quantitative equities, multi-asset and alternative asset class strategies.

Janus Henderson has approximately US$378 billion in assets under management (at 30 September 2018), more than 2,000 employees, and offices in 28 cities worldwide. Headquartered in London, the company is listed on the New York Stock Exchange (NYSE) and the Australian Securities Exchange (ASX).

This press release is solely for the use of members of the media and should not be relied upon by personal investors, financial advisers or institutional investors.

Issued in the UK by Janus Henderson Investors. Janus Henderson Investors is the name under which Janus Capital International Limited (reg no. 3594615), Henderson Global Investors Limited (reg. no. 906355), Henderson Investment Funds Limited (reg. no. 2678531), AlphaGen Capital Limited (reg. no. 962757), (each incorporated and registered in England and Wales with registered office at 201 Bishopsgate, London EC2M 3AE) are authorised and regulated by the Financial Conduct Authority to provide investment products and services. Janus Henderson Investors Europe S.A. (reg no. B22848) is incorporated and registered in Luxembourg with registered office at 78, Avenue de la Liberté, L-1930 Luxembourg, Luxembourg and authorised by the Commission de Surveillance du Secteur Financier. Henderson Secretarial Services Limited (incorporated and registered in England and Wales, registered no. 1471624, registered office 201 Bishopsgate, London EC2M 3AE) is the name under which company secretarial services are provided. All these companies are wholly owned subsidiaries of Janus Henderson Group plc. (incorporated and registered in Jersey, registered no. 101484, registered office 47 Esplanade, St Helier, Jersey JE1 0BD). © 2018, Janus Henderson Investors. The name Janus Henderson Investors includes HGI Group Limited, Henderson Global Investors (Brand Management) Sarl and Janus International Holding LLC.